Written by : Knowledge Centre Team

2021-06-15

871 Views

Share

What is retirement? It’s not like you can no longer bear the burden of professional work. You may even be in the best shape of your professional life. Your children are settled and perhaps earning their place in the world, you have achieved almost all financial goals of your life, except the legacy plan.

So, what is retirement really? Is it just a break from professional work?

If you look at it practically, no one stops you from continuing your profession for a few more years. But, one thing is certain, you no longer need to work for money anymore.

Thus, retirement may not be just a break from the work, but it is when you no longer depend on the income from your work. You can retire anytime once you have built a large enough corpus to take care of your post-retirement life.

In this article, we will discuss:

You need to replace income to take care of your expenses after retirement. The monthly budget for your household will look quite different from today because of the following changes:

You may be paying your child’s school and University fees in your 40’s and 50’s but that will cease when your child grows up. Ditto for children’s living expenses. Children grow up, start earning and living on their own. All the expenses about their lifestyle would come down to zero after a certain age.

Costs of commuting, lunch and other expenses related to the workplace would also no longer exist as you spend more time at home and very little time outside. Lifestyle expenses may also see a cut if you prefer

spending your sunset years closer home with family and friends instead of touring the world or frequently going on weekend trips.

The only major cost that could still burn a hole in your pocket is healthcare. Considering empirical evidence, inflation in the food and healthcare segments has been higher than the overall average rate of inflation. Moreover, the probability of you and your spouse needing more medical attention in old age is higher. Ergo, not only an increased wallet share but also the impact of higher inflation should be considered.

The estimated cost of living for you and your spouse is usually about 20-30 % of your monthly income. The remaining money is either spent as a lifestyle cost or saved for future needs.

So, if you are earning Rs. 1 lakh now you are spending about Rs. 20 - 30,000 on yourself and your spouse. This is the amount that will translate into personal expenses post-retirement as well.

This amount adjusted for inflation (5% p.a.) could go up to Rs. 90,000 in 30 years. So, if you are 30 years of age now, this is the amount you will need to start your retirement at 60. However, if you wish to retire at 50, you may withdraw a lower amount, i.e., approx. Rs 80,000.

But you will have a longer retired period to take care of, plus you may still need to take care of a few financial goals. Thus, if you can secure an income slightly higher than Rs. 90,000, say Rs. 1 lakh after your retirement, you may have an easier life ahead.

Also, this income has to take care of inflation in the future. So, every year, you should be able to withdraw a higher amount. To achieve such a post-retirement income starting at the age of 50, you will need a corpus of about Rs 2.8 crores.

If the inflation and rate of interest figures remain the same, saving about 35% of your salary should be enough to build an adequate retirement corpus for you in 20 years. Meaning, you can replace your current income within 20 years if you save 35% of your income towards this goal.

Learn why should you consider inflation while planning for retirement.

The next natural question is, ‘where to invest?’ So, here are the best retirement saving plans you can explore:

If you are a subscriber to any of these retirement schemes, you are already contributing 10 – 12% of your income towards your retirement. With NPS you can contribute up to Rs. 50,000 more each year, free of tax. However, to invest more you will need other investment options.

As a self-employed investor, as well, you can invest in an NPS Tier-I account. The limit for self-employed investors is 20% of annual income. Thus, you will need to allocate only the remaining 15% to other investment options.

Invest 4G, offered by Canara HSBC Life Insurance, is one of the most versatile retirement investments plans you can use. Your money is invested in both debt and equity instruments based on your allocation.

Invest 4G allows you to gain from the dynamics of the financial markets using automated portfolio management strategies. When you are young, you can invest aggressively in equity-oriented funds and then gradually move your money to safer debt funds. Thus, Invest 4G ULIP plan gives you the most tax-efficient way of building your retirement corpus.

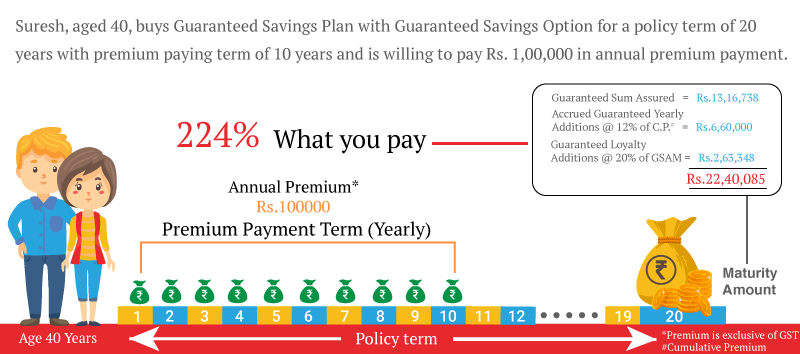

Another option for you to fill the gap in your retirement funding is through Guaranteed Savings Plan from Canara HSBC Life Insurance. As the name suggests the maturity benefits in this plan is guaranteed. So, you can estimate your plans maturity value beforehand.

Learn more about Guaranteed Savings Plan.

You will need to use monthly income plans to convert your corpus to regular income after you retire. The following two retirement saving plans are best suited to safely provide you with a long-term income stream:

Wherein you invest for 10 years and defer the pay outs by another 5 years. You can also decide to receive a lump sum instead of income streams. The plan offers guaranteed regular income for lifetime to meet post retirement options under Guaranteed Life-long Income option. Under this option, you can also cover your spouse, thus, securing both of your lives. With this plan, you can prepare for early retirement as it will give you that extra income to help you take care of both long-term and short-term financial goals.

You can park your lump sum corpus in this plan and convert it to income either immediately or after few years. Choose from a variety of annuity options and get guaranteed lifetime income, which will be directly credited to your bank account. This plan is a smart way to ensure that you have a regular and guaranteed income stream to help your post-retirement needs.

Learn more about Pension4Life Plan.

You can hold these plans jointly with your spouse so that the pension continues after your demise. The income streams, called annuities, are paid till the end of your life and then to your spouse. The fund value would then be given as a lump sum amount to the nominee.

Replacing income is essentially planning for retirement so that your lifestyle continues as is even after your full-time employment comes to an end. Your savings would then work as a financial nest that would give you predictable monthly income so that you never realize that you are not employed any more. At the same time, you can lead a cosy retired life reading your favourite books and watching all those movies that you never had time for, earlier.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.