Written by : Knowledge Centre Team

2021-01-18

871 Views

Share

Savings and investment are two different concepts that appear to be highly confusing in the eyes of many. You may think both saving and investment means the same. However, this is exactly where you go wrong. Both saving and investment are based on different ideologies and serve different purposes. A careful perusal is what’s needed in the first place before you decide on choosing the best saving plan. And at Canara HSBC Life Insurance, you can choose the best savings plan as per your life goals to save or invest.

The fundamental aspect of saving and investing money is to understand what comes first.

Saving money is the act of parking money in safe and liquid accounts or securities. Whereas investing money means using it to buy a productive asset-backed by some safety. Stocks, bonds, or even real estate makes for effective investment tools.

Now that the difference is understandable, the next major question would be when to save or invest and how much to save or invest. Saving comes before investment as a golden rule. Only when you have enough money saved to cater to your needs, you should think of investing it.

To save for a secure and safe future – a savings plan is the right tool as it offers a life cover along with a saving avenue. You might feel confused as you come across different saving policies and plans that provide you with the best way to save your wealth. However, at Canara HSBC Life Insurance, you would be assured that your savings are put into the best policies and plans that allow you to make disciplined savings.

It has the best saving plans and policies be it traditional investment plans or the new-age and current policies. These plans are conventional and different from the unit-linked insurance plans. There is no role of capital markets; hence, no market linkage. The insurance laws govern the working of such policies.

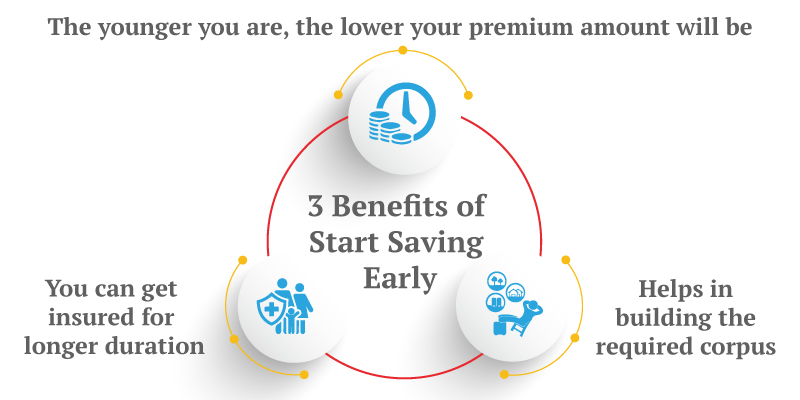

Buying the best saving plan can help you with the following:

These plans require money to be locked-in for almost 10-20 years, and there is no way to withdraw the amount before the term gets over.

Nonetheless, saving plans also aim to offer their customers tax benefits, terminal illness benefits, and also cover death benefits. These life insurance plans are futuristic and promise nothing but financial security for your family.

However, before choosing the best saving policy, remember to be sure of the following factors that ought to determine your decision to save in a particular plan/policy:

Canara HSBC Life Insurance helps you grow your money and accomplish your financial goals through a systematic investment procedure. The returns are payable to the beneficiaries depending upon their needs and the preferred plan.

If you are looking for comparatively modern plans in their approach, then Canara HSBC Life Insurance provides its customers with various saving plans and policies that suit the distinct needs of each customer. Saving plans resemble life insurance products and yield steady returns throughout the term.

The possibilities that they provide for you to save your money are immense.

Your rationale behind saving and investing might be different. Both the new ULIP saving schemes and traditional plans offer distinct benefits. ULIPs focus on wealth creation by encouraging capital markets’ involvement while traditional policies go unaffected by the same and make for a safer alternative. However, to each it’s own. What is necessary here is to know the correct balance between saving and investing. With the best saving policies from Canara HSBC Life Insurance, you get to choose the one that matches your aspirations and expectations.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.