Locate branch

Resume journey

Pay Premium

Contact us

Unit linked insurance plans or ULIPs are amazing investment products from life insurance companies. These plans not only enable you to save tax every year but also provide you with highly customisable investment plans.

A ULIP plan has multiple ‘unit-linked funds’ where you can allocate your invested premium. For example, Invest 4G plan from Canara HSBC Life has seven different funds for you to invest your money into. You can choose to invest your money in the following fund strategies:

- In any single unit-linked fund

- In a fixed ratio of multiple funds

- Using a portfolio management strategy

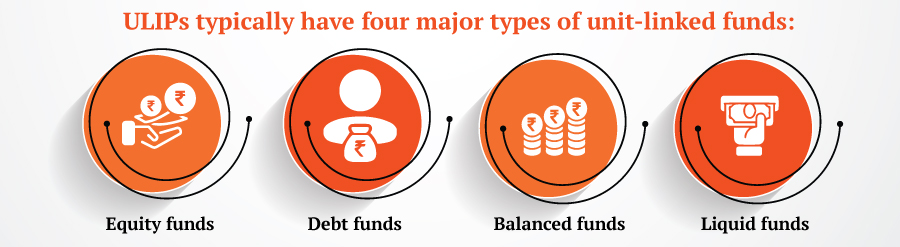

Various Unit Linked Funds in ULIPs

Equity funds are up to 95% equity stocks and securities, and 5% liquid assets and cash. Thus, carry the highest investment risk.

Debt funds are up to 95% long term debt securities, like bonds, Gilts and corporate debt, while 5% is liquid assets or cash. Thus, have lower risk, and offer steadier returns than equities.

Balanced funds have a dynamic allocation between long term debt and equity securities. Equity allocation in a balanced fund can range anywhere from 60% to 90% depending on market condition.

Since the asset ratio keeps on changing in these funds, the risk-return profile of the fund is also dynamic. However, for long-term investors, the profile should be medium-risk.

Liquid funds invest mostly into cash securities such as T-bills, commercial papers, money markets and ultra-short-term bonds (less than a year maturity). Liquid funds carry the least investment risk due to their asset profile.

These funds are best when you want to preserve the value of your investment in the short run. For example, as you approach the goal or in the final years right before maturity.

What is Premium Redirection?

Premium redirection is when you want to change how your upcoming premium should be allocated to different funds.

For example, you chose to direct 100% of your investment premium to an equity fund in the ULIP plan. After a few years, you want the premium to be split between an equity and a debt fund in 50:50 ratio.

This transaction is counted as a premium redirection in ULIP. With Invest 4G plan you can redirect your premium free of cost at least once during the policy year.

Effects of Premium Redirection on ULIP?

Premium redirection can impact your portfolio’s future allocation and risk profile. However, depending on the features you have been using, there could be different impacts.

For example, Invest 4G plan offers four automated portfolio management strategies. If you are using one of these strategies to manage your portfolio, premium redirection stops the automatic portfolio management.

Portfolio Management Strategies vs Premium Redirection

Invest 4G plan offers the following four portfolio management strategies:

- Systematic transfer

- Return protection

- Auto fund rebalancing

- Safety switch option

Except for the safety switch option, the rest of the strategies work throughout the life of the policy. Safety switch option, even if you opt at the beginning of the policy, works only in the last four policy years.

When you redirect the premium in the middle of the policy period, whichever portfolio management strategy is active will stop to operate.

For example, you are investing Rs. 1 lakh a year in a 15-year ULIP plan. You chose the auto fund rebalancing option to manage your portfolio at the time of starting the policy.

In the fifth policy year (after paying the fifth year premium), you submit a request to redirect your future premiums in the fourth month.

The policy will implement your request upon the receipt of the next annual premium; i.e. the sixth premium on the policy. So, from the sixth premium payment, the auto fund rebalancing strategy which rebalanced your portfolio every three months will stop.

In case you had opted for a monthly premium payment, the change would be effective from the fifth month in the fifth policy year itself.

When to Redirect Your Premiums?

In the normal course of life, you may not need to redirect premiums, especially if you are using one of the portfolio management strategies. However, insurance is a long term commitment and situations may change over time.

The only legitimate scenarios when you may have to intervene and change your usual allocation is when you:

- Had been investing heavily in equity but now expect to withdraw the money soon

- Had been investing in debt funds but markets are skewed and you see an opportunity you cannot miss

Whichever scenario applies to you, always remember the reason for starting this investment. If it was to meet a particular goal, that is what your primary focus should be. If it was to gather wealth, perhaps one or two interventions wouldn’t harm.

But do keep in mind that proven strategies work better in the long run than occasional interventions.

ULIP Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling ULIP insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Don't Just Survive, Thrive

Guaranteed Assured INcome

- 3 Plan Options

- Life cover + Guaranteed benefits

- Total Premiums at maturity

- Early income from 2nd policy year

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Recent Blogs

Why Ulip Is The Best Tax Saving Investment

02 Aug '24

874 Views

With the advent of technology, tax saving has been simplified in many ways and you can buy an insurance online at your ease. Before, buying an insurance make sure that you plan

Read More

Ulip

Why Ulip Is A Better Investment Option For Long Term Wealth Creation

02 Aug '24

870 Views

If you are looking for a reliable option that helps you to generate wealth in the long run, then ULIP is the perfect choice for you.

Read More

Ulip

Why One Should Not Exit Ulips After The End Of Lock In Period

02 Aug '24

880 Views

A host of financial products are available in the market catering to people with different financial goals and return expectations. People looking to financially secure

Read More

Ulip

Why you must not surrender your ULIP Policy?

02 Aug '24

870 Views

Life insurance is a rather unexplored topic and people have several misconceptions and confusions around it. This blog hopes to help clear your insurance related doubts.

Read More

Ulip

Why A Unit Linked Plan Is A Must For Stable Fund Generation

02 Aug '24

870 Views

It's tax saving season and most of us are trying to choose investments that also generate good returns. Here's why ULIPs make the cut.

Read More

Ulip