Locate branch

Resume journey

Pay Premium

Contact us

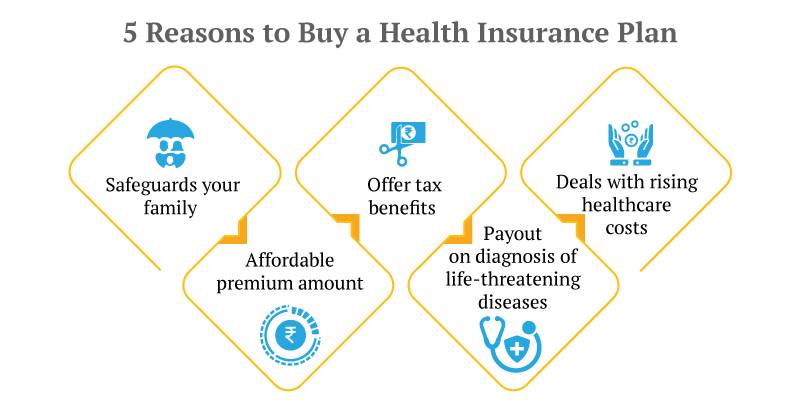

Health insurance, as the name suggests, helps you financially against all kinds of health issues, or at least that is the expectation. However, health insurance is designed to work as a tool to bring your financial life back on track after an emergency:

a. Which relates to your health.

b. It affects your life such that you must seek remedial measures.

c. You need to spend a significant sum to regain your normal life.

Should you Worry About IVF Cost?

Before you discard your existing health cover and start looking for one that covers IVF costs, understand if you need it. In medical terms, IVF is a way to resolve pregnancy woes. That means IVF itself is not a medical condition and doesn’t put you at major health risk.

However, the purpose of IVF is a successful pregnancy, that is, childbirth.

Childbirth or maternity expenses are covered by almost every family floater health insurance plan. Even better, your employer’s group medical insurance would offer to help with the maternity costs.

So, while IVF itself is not a health risk, your health insurance will cover any side effects of IVF and related medical costs.

Also Read about Cashless Treatment

Risk Associated During the IVF Procedure

Although IVF is not covered by insurance, there are certain risks involved in IVF treatment that can be covered if you have an insurance plan. Here are some of those risks:

1. Multiple Births: In some cases, IVF may increase the risk of multiple births by transferring multiple embryos to the uterus. In such a case, the pregnancy carries a higher risk of early labour, which can sometimes be dangerous to the mother's life.

2. Miscarriage: Sometimes, complications during or post IVF treatment may cause miscarriage. The risk of miscarriage during IVF can be higher if the maternal age is high, and it may pose a risk to the mother’s life.

3. Cancer: Though not very common, there are certain studies that have suggested that specific medications used during IVF treatment may increase the risk of ovarian tumours.

The mentioned risks can affect the life of the mother who is undergoing IVF treatment.

Types of Health Insurance Plans

You will find two different kinds of medical issues or illnesses – one which requires hospitalisation, or surgery and medication for recovery, and two which could be life-threatening even with treatment.

There are two different types of health insurance plans:

a) Defined Contribution Health Plans

The health insurance coverage you have for your entire family and the Mediclaim cover you receive through your employer fall into this category. Defined contribution means the premium cost for health insurance is defined. However, the benefit will depend on the actual expense.

The cost of IVF and similar treatments, if covered, will fall under this type of health insurance plan.

b) Defined Benefit Health Plans

A little less popular, yet equally important, these plans help you against life-threatening illnesses like cancer. This is why they are also called critical health insurance plans. You can buy a critical health cover as a rider with your term or health insurance plan.

These health plans have a defined benefit amount, meaning you will receive a fixed sum upon diagnosis of a covered illness. The amount you spend on treatment doesn’t affect your benefit from the plan.

Since IVF treatment is not a life-threatening situation, critical health plans are unlikely to cover this cost or condition.

You can cover maternity and related expenses with a family floater health cover (defined contribution plan). These plans will also cover the newborn from day one.

With critical health insurance you have a few options:

Include as a Rider with Term Insurance

Term insurance plans generally include terminal health cover by default. So, the term insurance plan works both as a life cover and critical health cover.

Buy as a Separate Cover

If you decide to buy critical health cover separately, you have the following three options:

a. General Critical Health Insurance: Covers terminal stages for all life-threatening diseases

b. Cancer Insurance: Covers all stages of cancer

c. Heart Insurance: Covers all stages of heart-related issues

Ideally, your contingency portfolio should include both plans.

Features of Critical Health Plans

You need to look for the following features in critical health insurance:

1. Increasing Cover

The sum assured under the plan should increase overtime to keep up with the rising costs.

For instance, if you opt for the Canara HSBC Life Insurance Health First Plan for your wife, you can get this feature. Your initial Sum Assured will grow by a simple rate of 10% per annum from the 2nd policy year till the date you make your first claim.

2. Return of Premium

It means your cover does not cost you anything if there was no claim on the plan. So, all the premiums you have paid for the cover return to you if the plan expires without a claim.

This will take care of the ongoing health and medical expenses involved in cancer treatment. Hence, you can easily get cancer treatment without any financial burden.

3. Premium Waiver Benefit

This feature ensures that you don’t have to worry about premium payments after the diagnosis of a critical illness.

If you opt for this feature, the premiums after the death of the policyholder shall be paid by the Insurance Company. The term plan won’t end after the policyholder’s death and will continue till full term.

As far as your financial needs go, health insurance must be on priority. Whether you are looking for IVF cover or not, a family floater and critical health are must have covers. These life insurance plans will ensure long-term financial safety for your family.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

Recent Blogs

When is the right time to buy a health insurance plan?

02 Aug '24

872 Views

A health insurance plan has become quintessential in the wake of COVID-19. It is always better to stay guarded for uncertainties and buying the best health plan can help you stay prepared

Read More

Health Plan

What is a Comprehensive Health Insurance Plan?

02 Aug '24

874 Views

Comprehensive health insurance is a perfect mix of relevant health insurance plans to offer safety from the hospital as well as major treatment expenses. Discover how to create your comprehensive health cover…

Read More

Health Plan

What is Incurred Claim Ratio?

02 Aug '24

875 Views

Incurred Claim Ratio refers to the total claim paid by an insurance company in a financial year to the total premiums collected. Learn the difference between incurred claim ratio and claim settlement ratio.

Read More

Health Plan

What is Cashless Treatment?

02 Aug '24

875 Views

Cashless treatment is when the entire hospitalisation expenses are settled by the insurance company itself. The policyholder do not have to pay anything to the hospital as the expenses are managed by the insurance company.

Read More

Health Plan

What is Not Covered in your COVID-19 Health Insurance Plan?

02 Aug '24

873 Views

Buying the best health insurance plan online will help you financially if you are diagnosed with COVID-19. However, you must know what expenses are not covered under your COVID-19 health plan.

Read More

Health Plan

Popular Searches

- Family Health Insurance Plan

- What is Health Insurance?

- Health Insurance For Parents

- Health Insurance Tax Benefit Under 80-D

- Health Insurance Facts

- Difference Between Life and Health Insurance

- Difference Between Life and Health Insurance

- Incurred Claim Ratio

- What is Copay in Health Insurance?

- What is Cashless Treatment?

- Accidental Cover in Saral Jeevan Bima

- Accidental Cover in Saral Jeevan Bima

- Tips to Buy Health Insurance

- Short Term Health Insurance Plan

- When Should You Buy Health Insurance?