Locate branch

Resume journey

Pay Premium

Contact us

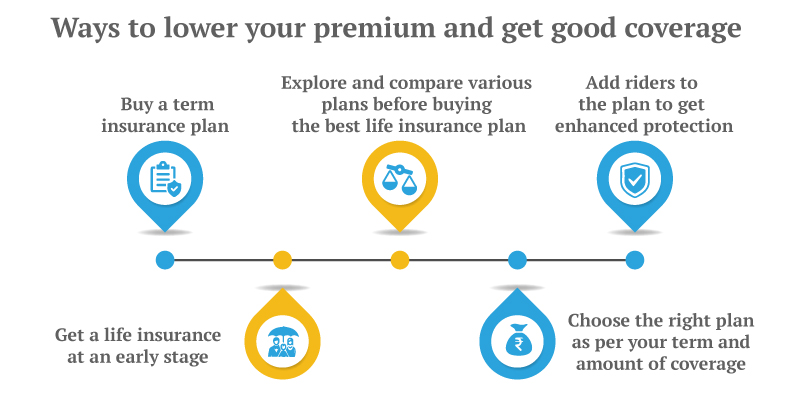

Buying a life insurance is one of the critical financial decisions of your life and should ideally be one of the first investments out of your income. That also means the moment you start earning you need to decide and buy the best life insurance cover in your budget.

However, let’s not forget that life insurance is a long-term investment. Your first life insurance plan, most likely a term insurance cover, should stay with you till retirement. Thus, if you started earning at the age of 25, you should get a term insurance cover for the next 35-40 years.

That is a very long time, and your life could change dramatically within the first decade. So, the first plan should be such that you can stick with it for a lifetime.

If the premium of the life insurance plan has been a criterion for your investment decision, you should spend some time understanding it. Otherwise, the lowest premium will often sound like a better deal than even the best life insurance plan.

5 Quick Steps to Calculate Life Insurance Premium

You can calculate life insurance premium using the online calculators for the plan. For other plans, you will need to either discuss with an advisor or check with customer care. Using an online calculator is a simple step by step process:

Step 1

Provide your name, contact, lifestyle habits (smoker, non-smoker, alcohol consumption) and income details.

Step 2

Select the amount of cover you need or the amount of money you plan to invest. Ensure that you choose an adequate amount so that you stay protected all the time.

Step 3

Check the base annual premium and select the mode of premium payment (monthly, quarterly annually). Some of the life insurance plans, mostly, term insurance plans like iSelect Smart360 Term Plan also offers limited premium pay option.

Step 4

Select add-on benefits, such as goal protection option (in case of investment life insurance), accidental death and disability covers. Adding riders to your life insurance plan enhance the coverage.

Step 5

Select the premium payment term for the policy and check the final premium that you will have to pay as per the premium payment frequency chosen by you.

Why Should you Calculate Life Insurance Premium?

Premium calculation is an important step in the process of buying a life insurance plan. Calculating the plan’s premium also allows you to compare the plan with other similar investments and helps you choose the best life insurance for your goal.

It also helps you determine if you can afford the full investment in your future goal. If not, you can reduce the plan’s expected maturity value to bring the contribution within budget.

Also, remember that situations specific to individual conditions, like family health history, etc. are considered only after you submit the application. The premium amount shown to you before filing the application is a general premium for the age group with similar conditions.

In case of a pre-existing health condition, the insurer may charge a higher premium for the same amount of cover. A large number of investors leave the application incomplete at this stage. However, you should remember that your pre-existing health condition or family history makes your family vulnerable to the risk of losing you early.

Thus, the fractional increase in the premium amount is a necessity you should still consider buying the plan.

7 Factors Influencing your Life Insurance Premium

Every life insurance plan comprises of a protection element and an investment element in different proportions. Few insurance plans like term life cover with terminal illness covers are pure protection plans without any investment component.

Learn these 14 reasons you might be paying a higher premium.

Thus, the premium for these plans is affected by the factors which increase the risk to your life or health. The most important factors influencing the risk premium of your life insurance plans are:

1. Your Age

Age is the first factor that is considered for life insurance premiums. First and foremost, your age will define if you are eligible for the plan. Most life insurance protection plans, like term and health insurance plans, allow you to buy the policy if you fall within a specific age range. For example, between 18 to 65 years.

Second, as you grow older, your risk premium for the life insurance cover increases. That is because the risk premium is based on mortality rate (rate of death) among the specific age group you belong to.

For example, the term insurance premium for a 22 years old would be lower than a 35-year-old male.

2. Your Health Condition

Your present health is an important parameter deciding your life insurance premium. Health conditions such as height and weight ratio (BMI), pre-existing diseases can increase your risk of early death. Thus, you may have to pay a higher risk premium for the same amount of cover.

3. Health History of your Family

Even if you are healthy at the time of buying the life insurance, you may have a long family history of specific diseases. In such, cases too, your life insurance premium is expected to rise.

4. Your Occupation

Life insurance underwriting principles divide occupations into three to four categories, depending on combination of physical and mental stress on the job. If you are working in a role that involves dealing with heavy machinery, working in a dangerous environment, your life insurance premium would be higher.

If you have a desk job you may have a slightly lower risk. Hence, the premium that you have to pay will be lower.

5. Geography or Location

Location is also a consideration while estimating your life insurance premium. Urban centres, like metro cities and state capitals, may enjoy a lower premium than a rural area.

6. Lifestyle Choices & Habits

Lifestyle choices like cigarette smoking or alcohol usage also affect your risk to life and thus the life insurance premium.

7. Other Factors Deciding your Premium

You can invest in life insurance plans to achieve your future financial goals as well. In such cases, the risk premium is only a small component of the total annual premium you pay. Your life insurance premium will also consider the following factors:

- Your future goal amount

- Time: Policy Term

- Investment Tenure: Premium Payment Term

- Riders and additional benefits you selected

These factors determine the investment part of the total premium of your plan. So, before you buy a life insurance plan, calculate the premium to figure out how much you will have to put aside for your premiums. Also, you can prepare a monthly budget to accommodate the premiums without much hassle. However, this is possible only when you know beforehand how much amount you will have to pay. There are a lot of reasons you should check your insurance premium before making any decision. Take the help of online life insurance premium calculators to figure out your premiums and to choose the best life insurance plan available as per your financial circumstances, and goals.

Life Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Recent Blogs

How to Choose the Best Savings Plan in India?

02 Aug '24

889 Views

Read More

Life Insurance

Reasons Why Stay At Home Parents Need Insurance Too

02 Aug '24

873 Views

Work hours extending beyond the standard nine-to-five grind, no provision of leave, juggling work between multiple departments, and no payment-welcome to the life of a stay-at-home parent.

Read More

Life Insurance

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance

02 Aug '24

872 Views

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance introduces 1 day settlement of death claims, with 98.12% claim settlement ratio

Read More

Life Insurance

Life Insurance The Key to Happiness Post-Retirement

02 Aug '24

870 Views

How does your retirement planning tackles the question of passive income? Can you set yourself free from the need to work after retirement?

Read More

Life Insurance

9 Ways you Can Use Life Insurance in your Life

02 Aug '24

870 Views

Benefits of life insurance span throughout all important stages of your life. Whether it is the financial safety of family or your own retirement uses of life insurance plans are far more than it seems…

Read More

Life Insurance

Popular Searches

- Term Life Insurance

- Whole Life Insurance

- Critical Illness Insurance

- Accidental Death Benefit Rider

- Compare Life Insurance Quotes

- Best Life Insurance Companies In India

- Factors Affecting Life Insurance Premiums

- Insurance For Tax Savings

- Life Insurance For Children

- Life Insurance Rider

- Life Insurance Plans

- Types of Life Insurance

- Term Life Insurance Tax Benefit

- What is Insurance?

- Life Insurance Premium