Locate branch

Resume journey

Pay Premium

Contact us

Few long-term investments are as safe and versatile as life insurance plans. If you have been investing in any of these long-term investment plans, including a life insurance policy, you can use the corpus for another asset – a house.

Home is one of the essentials for life. Thus, home buying could be a financial goal you’d like to achieve in your life, and the sooner the better. Not only that, but the house is also a long-term asset, which grows in value gradually and can even become a source of funds in your retirement.

So, how can you fund your house purchase dream?

Here are the two possible ways:

1. Define the goal and start investing now

2. Use your existing investments to achieve the goal

1. Defining the Home-Buying Goal

Home buying goal is so flexible with several options that you really have to sit down and make notes, and perhaps you should. However, for the sake of simplicity let’s just take one scenario:

“You want to buy your first house, and you want to do it as soon as possible”

You can either buy a house using a bank loan or buy a house completely out of your pocket, that will be your choice. However, in both cases, the value of your dream property will define the financial goal for you.

For example, assume if you wish to buy a property that costs Rs. 60 lakhs today:

- Rs 60 lakhs + 12% of Rs 60 lakhs (approx. Rs. 70 lakhs) should be your financial goal if you want to buy out of pocket

- 20% + 12% of Rs 60 lakhs (approx. Rs 20 lakhs) should be your goal if you wish to use a home loan for the purpose

Using Existing Life Insurance Policies for the Goal

Life insurance policies like unit-linked insurance plans and endowment plans acquire cash value as you continue investing in these policies. So, if you have started a policy 10 – 15 years ago, the policy may have acquired enough cash value to help you achieve your home buying goal.

If not, you can continue investing in the policy and start a new investment as well to achieve your goal. Life insurance plans like endowment and money-back plans acquire higher cash value as they near their maturity.

How does Cash Value Work?

You can use your life insurance policy’s cash value in two ways:

- Surrender the policy

- Borrow from the policy

If you surrender the policy, you will get 100% of the cash value of the policy. However, the policy will cease to exist, and you may lose a chunk of your life cover.

Borrowing against the policy or from the policy will give you only 80% of the cash value. But it has other advantages:

- Low rate of interest on the loan

- The policy continues and you will still receive the balance maturity value

- Life cover continues

- You can repay the money for the policy and enjoy an even lower outflow towards interest payments

Remember cash value of the policy is only a fraction of the maturity value. So, it does not make much financial sense to surrender the policy in the final few years as you may lose a larger chunk of the bonus additions which are payable on maturity.

Learn 5 ways to cash out a life insurance policy.

When to Use the Policy Cash Value?

You should use your policies cash value only under the following circumstances:

- The policy will mature after more than three years

- You cannot withdraw from the policy

For example, if you have a unit-linked life insurance plan you can withdraw money from your policy before maturity. So, if withdrawals are enough to meet or cover more than 80% of your goal no need for using cash value.

However, in case, which is very likely, you do not have a long-standing life insurance policy in your portfolio, you can start investing today.

Invest in Life Insurance Plan for Home Buying Goal

Investing in a life insurance policy to meet a large financial goal is nothing new. You can use life insurance plans to meet important and large financial goals such as higher education for your child. So, the home buying goal should not be too different.

However, you would like to expedite the home buying goal, even with a new investment route. And before you go on investing here’s why life insurance plans could be the best instruments for this goal:

- Additional life cover, i.e., additional financial safety for your family

- Only investment plans with an option to protect the goal

- You can invest both aggressively in equity and play safe with guaranteed plans

- Tax-saving on invested money and tax-free maturity value

So, here are few investments plans you can consider:

1. Unit Linked Plans – Invest Aggressively or Play Safe

Unit linked insurance plans or ULIPs are versatile investments that let you invest in a mix of equity and debt funds. You can also choose to invest only in equity funds or only debt funds, depending on your risk appetite and preference.

Here’s how the best online ULIP plans like Invest 4G from Canara HSBC Life Insurance facilitate equity investors:

- Manage your portfolio risk automatically

- Use automated strategies to always benefit from market movements

- Bonus additions for long-term investments

- Switch anytime between funds

- Automatically and systematically transfer your equity portfolio to debt in the final few years of the policy

- Partial withdrawals are allowed after a five-year lock-in period in the policy

- Protect your home purchase goal for your family from your untimely demise

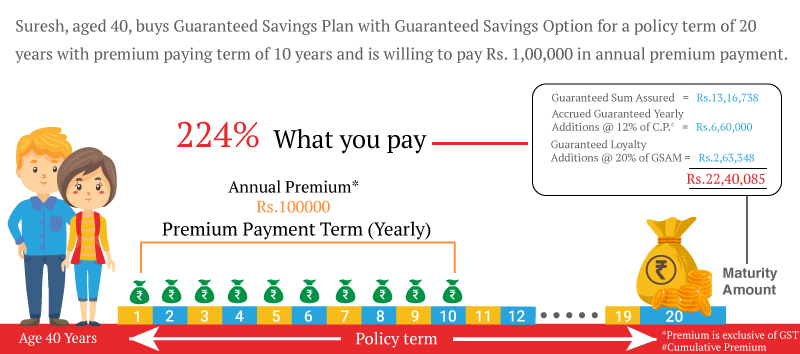

Guaranteed Savings Plans

A Guaranteed Savings Plan is an endowment plan with guaranteed maturity value. You can estimate your guaranteed maturity value at the time of starting your investment. Or you can choose a goal and start investing accordingly in this plan.

This plan has:

- Guaranteed bonus additions for regular and long-term investors

- Tax benefits on investment and maturity value

- Goal protection feature

Goal protection or premium protection option allows your investments to continue even after your untimely demise. The insurer will continue to invest the due premiums on your behalf and will pay the maturity value to the family. In the meanwhile, your family will also receive the guaranteed life cover amount upon your demise within the policy term. Thus, the plan fulfils their immediate and future financial need with this option, and your family can still have a house of their own.

Life Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Recent Blogs

How to Choose the Best Savings Plan in India?

02 Aug '24

890 Views

Read More

Life Insurance

Reasons Why Stay At Home Parents Need Insurance Too

02 Aug '24

873 Views

Work hours extending beyond the standard nine-to-five grind, no provision of leave, juggling work between multiple departments, and no payment-welcome to the life of a stay-at-home parent.

Read More

Life Insurance

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance

02 Aug '24

872 Views

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance introduces 1 day settlement of death claims, with 98.12% claim settlement ratio

Read More

Life Insurance

Life Insurance The Key to Happiness Post-Retirement

02 Aug '24

870 Views

How does your retirement planning tackles the question of passive income? Can you set yourself free from the need to work after retirement?

Read More

Life Insurance

9 Ways you Can Use Life Insurance in your Life

02 Aug '24

870 Views

Benefits of life insurance span throughout all important stages of your life. Whether it is the financial safety of family or your own retirement uses of life insurance plans are far more than it seems…

Read More

Life Insurance

Popular Searches

- Term Life Insurance

- Whole Life Insurance

- Critical Illness Insurance

- Accidental Death Benefit Rider

- Compare Life Insurance Quotes

- Best Life Insurance Companies In India

- Factors Affecting Life Insurance Premiums

- Insurance For Tax Savings

- Life Insurance For Children

- Life Insurance Rider

- Life Insurance Plans

- Types of Life Insurance

- Term Life Insurance Tax Benefit

- What is Insurance?

- Life Insurance Premium