Locate branch

Resume journey

Pay Premium

Contact us

Do you plan to buy a life insurance policy, because it offers financial cover to you and the family in case of some unpleasant happenings? Before finding the best life insurance plan, you must know the purpose of buying an insurance plan. Do you want to buy a policy to protect the family financially in case of your untimely death? Or you look at the policy as an aid to resolve issues such as:

- Payment of outstanding debts

- Aid to run house in case of loss of job

- A major contributor to a child's higher education?

- A combination of all or part of the above?

The purpose to buy a policy helps in evaluating the insurance amount you require for the fulfilment of the same. If you already own a life insurance plan, then it is important to know the benefit of buying an additional policy and what value will it add to the investments and financial security.

By having a purpose, you can buy the best life insurance plan that meets your requirements at an effective cost. It is also necessary to know for whom you want to buy an insurance plan. Who do you want to buy an insurance plan for?

- Yourself

- Spouse

- Child

- Dependents

Money can't fill the void your death will leave in the life of your loved ones. But it can work as financial assistance to them in your absence.

Documents for Buying Life Insurance Plan

Your application for a life insurance plan contains information largely under the following four heads. Thus, you will need to provide as many documents as well, to support your information:

- Proof of address: Aadhaar, Driving License, Passport

- Identity Proof: PAN card, Passport, Driving License

- Income Proof: Salary slips, bank statement, ITR

- Medical History: Any relevant medical report

Buying the Life Insurance Plan you Need

Understanding your financial and safety needs and finding the best suitable life insurance plan accordingly is what you need to do. Given below are a few steps and tips to break down your search and find the life insurance plan for your family:

1. Know Your Options

There are two types of life insurance plans:

- Pure protection plans

- Savings plans

Pure protection plans usually only work in case of an emergency. For example, a term insurance plan or health insurance plan. These plans have lower premiums but have a very important role to play in your family’s survival if anything happens to you.

Savings plans, like unit-linked insurance plans (ULIPs), endowment plans, child plans, retirement and pension plans are designed to help you achieve specific life goals. With these plans, you can hope to achieve your goal within the safety umbrella of a life cover.

For example, if you are saving for your child’s higher education, a child plan will ensure that your child gets the financial support you planned for her/him. In the case of your early demise, the plan continues to invest in your child’s goal and pays the maturity funds to the child as you intended.

2. Assess Your Insurance Need

Your insurance needs consists of two factors:

- Your family’s lifestyle and living costs (Covered by pure protection life insurance plans like term life insurance)

- Your family’s future goals (cover individually with savings plans)

The assessment of these two will let you know the premium amount you can pay regularly. Remember life insurance comes before investments. So, even if your income and expenses do not allow huge savings, at least the pure protection life insurance plan is a must.

The amount of cover in these plans should, however, depend on the financial need of your family. For example, a term life cover should be large enough to help your family maintain their lifestyle until the children grow up and start earning.

Or you can follow a simple rule of thumb and buy a term life cover at least 10 times your annual income. This will be enough to cover your family’s urgent financial needs for long enough for them to stand on their feet.

The financial goals will be covered individually with your savings plan investments.

3. Buy Life Insurance Online

With the availability of online insurance policies, you can find a suitable life insurance plan sitting on your couch or office table. You can check the premium cost of the life insurance plan you want to buy using the online premium calculators.

The calculators also help you compare:

- The cost of adding different features and benefits to your plan

- Premium amount for different premium payment tenures

- The premium cost of paying your policy premium in different modes

The online mode lets you compare different plans, discover the company’s performance and also interact with the customer service.

Learn how to buy a life insurance policy online.

4. Insurance Application & Premium Revision

One of the steps while buying an insurance plan is the application form. You may find that the life insurance application form is a quite detailed document. You need to provide information about your life, occupation, and medical history.

For a healthy individual with a normal medical history, the insurer may allow life cover without a medical examination. However, for most other cases it will be another necessity. If you have a medical condition or a family medical history of certain diseases the insurer may revise your final premium.

Although, this amount could be higher than the originally estimated premium cost, due to your medical history the life cover is even more important for your family. In case of wrong information or hiding a piece of relevant information from the application forms, your family may lose the claim settlement.

Other factors which may cause an upward premium revision after submitting a proposal are:

- Occupation

- Hobbies

- Adverse medical report

The medical examination that the insurer schedules for you is also an important step towards the financial safety of your family. It’ll help you find any medical condition you have been unaware of.

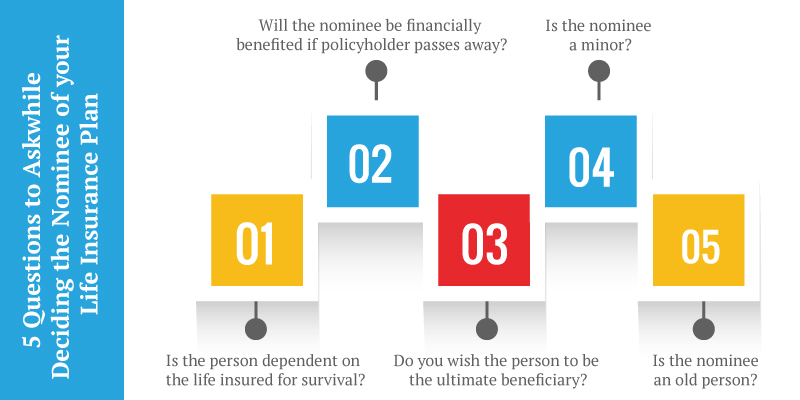

5. Select Your Nominee

At the time of applying for insurance, you need to share the name(s) of the nominee/beneficiary who would receive the sum assured after your death. In the case of a married person, the spouse automatically becomes the nominee. However, you have the option to add your children as a beneficiary.

Learn more about how to choose a nominee for your life insurance plan.

Frequently Asked Questions (FAQs)

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

You must provide salary slips or form 16 for the tax assessment of the current year as proof of income while buying a life insurance plan.

Yes. Along with your identity proof, you are also required to submit identity proof of the beneficiary as well to buy a life insurance policy.

For receiving the disbursal amount of the insurance policy, you need to submit a death certificate, claim form, policy bond, FIR copy, post-mortem report if required.

The insurance company sends an intimation letter along with the discharge voucher to the policyholder 2 or 3 months earlier from the date of maturity to make timely payment. You are required to return the duly signed policy bond and the discharge voucher to the insurance company for timely disbursal of the amount.

After assessing the requirement choose the best life insurance policy in India or a whole life insurance policy whichever suits you the best.

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

You must provide salary slips or form 16 for the tax assessment of the current year as proof of income while buying a life insurance plan.

Yes. Along with your identity proof, you are also required to submit identity proof of the beneficiary as well to buy a life insurance policy.

For receiving the disbursal amount of the insurance policy, you need to submit a death certificate, claim form, policy bond, FIR copy, post-mortem report if required.

The insurance company sends an intimation letter along with the discharge voucher to the policyholder 2 or 3 months earlier from the date of maturity to make timely payment. You are required to return the duly signed policy bond and the discharge voucher to the insurance company for timely disbursal of the amount.

After assessing the requirement choose the best life insurance policy in India or a whole life insurance policy whichever suits you the best.

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

You must provide salary slips or form 16 for the tax assessment of the current year as proof of income while buying a life insurance plan.

Yes. Along with your identity proof, you are also required to submit identity proof of the beneficiary as well to buy a life insurance policy.

For receiving the disbursal amount of the insurance policy, you need to submit a death certificate, claim form, policy bond, FIR copy, post-mortem report if required.

The insurance company sends an intimation letter along with the discharge voucher to the policyholder 2 or 3 months earlier from the date of maturity to make timely payment. You are required to return the duly signed policy bond and the discharge voucher to the insurance company for timely disbursal of the amount.

After assessing the requirement choose the best life insurance policy in India or a whole life insurance policy whichever suits you the best.

Yes. You are required to submit proof address that can be an electricity bill, house tax receipt, or a water bill to buy a life insurance policy.

You must provide salary slips or form 16 for the tax assessment of the current year as proof of income while buying a life insurance plan.

Yes. Along with your identity proof, you are also required to submit identity proof of the beneficiary as well to buy a life insurance policy.

For receiving the disbursal amount of the insurance policy, you need to submit a death certificate, claim form, policy bond, FIR copy, post-mortem report if required.

The insurance company sends an intimation letter along with the discharge voucher to the policyholder 2 or 3 months earlier from the date of maturity to make timely payment. You are required to return the duly signed policy bond and the discharge voucher to the insurance company for timely disbursal of the amount.

After assessing the requirement choose the best life insurance policy in India or a whole life insurance policy whichever suits you the best.

Life Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Recent Blogs

How to Choose the Best Savings Plan in India?

02 Aug '24

890 Views

Read More

Life Insurance

Reasons Why Stay At Home Parents Need Insurance Too

02 Aug '24

873 Views

Work hours extending beyond the standard nine-to-five grind, no provision of leave, juggling work between multiple departments, and no payment-welcome to the life of a stay-at-home parent.

Read More

Life Insurance

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance

02 Aug '24

872 Views

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance introduces 1 day settlement of death claims, with 98.12% claim settlement ratio

Read More

Life Insurance

Life Insurance The Key to Happiness Post-Retirement

02 Aug '24

870 Views

How does your retirement planning tackles the question of passive income? Can you set yourself free from the need to work after retirement?

Read More

Life Insurance

9 Ways you Can Use Life Insurance in your Life

02 Aug '24

870 Views

Benefits of life insurance span throughout all important stages of your life. Whether it is the financial safety of family or your own retirement uses of life insurance plans are far more than it seems…

Read More

Life Insurance

Popular Searches

- Term Life Insurance

- Whole Life Insurance

- Critical Illness Insurance

- Accidental Death Benefit Rider

- Compare Life Insurance Quotes

- Best Life Insurance Companies In India

- Factors Affecting Life Insurance Premiums

- Insurance For Tax Savings

- Life Insurance For Children

- Life Insurance Rider

- Life Insurance Plans

- Types of Life Insurance

- Term Life Insurance Tax Benefit

- What is Insurance?

- Life Insurance Premium