Written by : Knowledge Centre Team

2021-11-17

871 Views

Share

Risk is the basis of any insurance. In the case of life insurance, the risk is the likelihood that you are going to die within the policy term. The risk involved will decide the coverage you can be eligible for. The more the risk involved, the more will be the chances of you paying higher premiums.

Insurers assess your risk profile before providing you with life insurance. The basis of insurance is probability. Insurance is generally provided for those events whose probability of happening will not be very high. If there are high chances that something might happen to you, then you possess a higher risk for the insurer.

How much risk you possess for the company is based on a host of factors determined by the insurance company itself. One such factor is health. The risk that is external to you is already included while calculating the premium as it’s the same for all. But what plays a major part in differentiating premium rates is your health condition.

Your health plays a significant part in deciding your risk and ultimately the premium you will pay. The higher the risk, the higher will be the premium. Your general health parameters such as height and weight are checked along with specifics such as blood samples, etc.

For example, if you are overweight, you may be charged extra premiums as obesity brings with it certain health conditions.

Click here to Use - BMI Calculator

The process through which all these things are checked is called underwriting in insurance.

It is the process that is used by the insurance providers to determine the risks they will be taking by providing you with a life insurance policy.

Under medical underwriting, your overall health is evaluated by the insurance company based on your medical conditions. How is your health currently and what was your condition in the past, both are considered. This helps them to determine the following things

Underwriting especially medical is an integral part of insurance. The insurer has to make sure that you are not buying the policy when you know you are going to require medical care.

The process of medical underwriting is carried on by an underwriter. These underwriters work for the life insurance companies and help in determining as well as managing risks involved.

Now since we know what is the meaning of medical underwriting, let’s take a look at how it is done.

It involves three steps.

To buy any life insurance, the first step involves filling the application. In the application form, It asks you details such as your name, age, occupation. It asks you a detailed question about your medical history, current health, and lifestyle as well.

Once you enter the details, the application, it is transferred to the insurance company’s selected underwriter for him to check.

It is advised to enter all the asked details carefully and correctly in the application. The more information is missed the more time it will take to reach the underwriter.

Learn these 5 reasons why your life insurance application could be declined.

Underwriter for assessing your risk requires certain health details from you. Life insurance companies recommend various medical tests for you to take. The underwriter will generally require the reports of the following tests from you.

Your medical report is a confidential document and is usually shared with the insurer directly. After receiving the reports, the underwriter checks them with the help of the guidelines set.

After receiving the reports and the application, the underwriter then decides whether the company can provide you insurance or not.

If all your reports seem fine to the company, you are provided with an amount that you will pay as your premiums and how much coverage can they provide you.

All you have to do is to read the terms and accept or reject the policy. If the final decisions are as per your desire, you can accept the policy, sign and the policy will be in place.

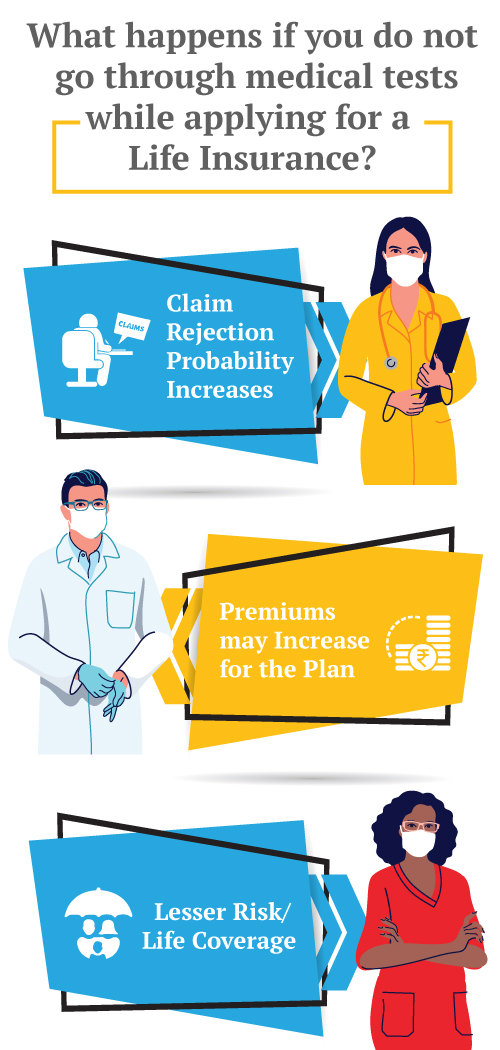

Some policies don’t involve underwriting. This policy becomes a good option when you don’t want to undergo various medical examinations or you already are in poor health. But these policies generally cost more than policies that involve underwriting.

Insurance companies provide certain life insurance plans which don’t require medical screening but if you have a pre-existing illness, then medical will be taken.

If you have no such condition and are healthy, it is generally advised that you go for a policy that involves medical underwriting.

We know how your health can affect your premium. If your lifestyle includes habits like drinking and smoking and you face constant health issues, it will mean that your risk probability is higher to the insurer. Having a high risk will lead to you paying higher premiums. No one likes to pay higher. So what could you do to lower your premiums?

For starter, you can start having a healthier lifestyle

Good health not only benefits you physically and financially, but it also attracts lower life insurance premiums. Exercising daily and caring for your health will be beneficial for you. Constant medical check-ups to monitor your health is also important

As per lifestyle habits are concerned, smoking is the cause of many chronic diseases such as cancer, etc. Avoiding smoking and heavy drinking can also help you attain good health.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.