Written by : Knowledge Centre Team

2021-04-22

871 Views

Share

Buying a life insurance plan is not as complicated or confusing as it once used to be. But often, the kind of lingo used by banks to differentiate between different types of products they offer can befuddle someone who is new to the world of finance and investment. The closest some people come to have a financial portfolio is to get life insurance for themselves or their family, but sometimes even something as simple as insurance comes with a myriad of clauses and categories that can make the average citizen dread going to the bank.

One such confusing and similar-sounding set of terms is that of ‘whole life insurance’ and ‘universal life insurance - they may sound almost synonymous to you, but their implications in the banking sector are quite differentiated.

To put it simply, whole life insurance provides coverage for your entire life, i.e., for as long as you live. This implies that even if you pay the premium amounts only for a specific and predetermined period of time, the death benefit that is promised by the bank will be valid for the remainder of your existence.

A whole life insurance plan is often recommended for people with families that have a lot of dependents, especially if the potential policyholder is the leading breadwinner of the family whose loss will be felt sorely in terms of finance. Whole life insurances can provide the peace of mind that the dependents will be taken care of if the policyholder dies an early and unfortunate death.

The amount accumulates over the years and becomes available to the policyholder or their dependents on maturity, by which time it would be significant enough an amount to cover whatever expenses the family may need after the death has occurred. The savings amount is also kept on a tax-deferred basis and can be borrowed if there is a need for it.

In this manner, whole life insurance helps an individual complete their long term financial goals for the entirety of their lives. Because it functions both as insurance and savings, banks tend to ask for higher premiums compared to ordinary term insurance.

Universal Life Insurance is different from an ordinary life insurance plan because it is far more flexible in terms of the death benefit amount, which you can increase or decrease depending on your health and your preferences.

Of course, to increase the assured sum that is your insurance cover, you have to undergo a thorough medical examination that assures the bank that you are in good health. Decreasing the coverage, which means paying fewer premiums, can be done without giving up the entire policy if you pay a small amount as surrender charges.

Learn more on increasing sum assured in a term insurance plan and how it can beat the inflation.

The flexibility also extends to the frequency of the payment. Under universal life insurance, you can pay the premiums at any time; even all at one go, if you prefer a lump sum. From this amount, a policyholder can withdraw smaller sums partially, mimicking the way investment components work in other insurance-savings plans.

The only con of universal life insurance is that if the policy starts performing poorly, you cannot expect growth - you may end up spending a lot of money as premiums to keep the cash-value amount to the highest, and backing outcomes with the risk of high surrender charges. However, if flexibility is one of your priorities, you should definitely choose universal life insurance.

People are often torn between the two, but both whole life insurance and universal life insurance are permanent life insurance policies that combine components of life coverage and investment. The main difference between the two types is flexibility.

While universal life insurance is far more flexible on many fronts, the assurance and consistency that a whole life insurance policy offers is a robust income replacement in case something happens to the policyholder and the dependents need to be taken care of.

Your choice between universal life insurance and a whole life insurance plan depends entirely on what you are looking for. If you are searching for a policy that offers consistency and an assured payout that is predetermined, you should not think twice before opting for whole life insurance.

But if you are a risk-taker who prefers flexibility or are someone who cannot afford to pay for a whole life cover, universal life insurance is the choice for you since it can adapt to your financial situation.

People whose professions do not assure a stable flow of income usually prefer to go for universal life insurance, while people with a large number of dependents choose whole life insurance. Whole life insurances are highly recommended for people whose largest incentive to purchase insurance is their concern for their family’s future. Also, there are term insurance plans that offer whole life option along with return of premium. If you opt for such a plan, it’s a complete win-win for you.

Learn why a whole life plan with ROP is the smarter way of buying life insurance.

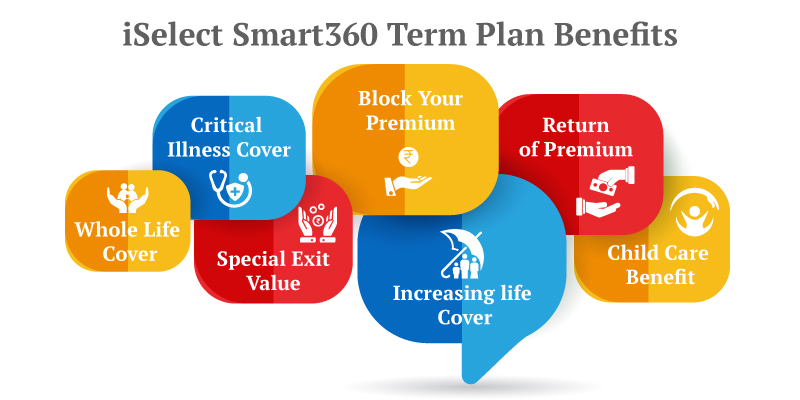

Canara HSBC Life Insurance offers term insurance plan with whole life option in India. iSelect Smart360 Term Plan comes with the following additional perks, which are helpful for anyone’s financial portfolio:

Purchasing a term insurance plan with a whole life option like iSelect Smart360 Term Plan can give your family the confidence to broaden their horizons without the fear of financial crisis. On the other hand, the flexibility of the universal life cover can give you options that whole life plans may not offer. At the end of the day, the choice between the two depends on what is best suited for your situation and family.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.