Written by : Knowledge Centre Team

2022-09-26

871 Views

Share

Public Provident Fund is a small savings scheme launched in 1968 by the National Savings Institute and the Ministry of Finance. The 15-year saving scheme was to bring the self-employed and unorganised sector employees to par with the organised sector workers. Public Provident Fund (PPF) is a long-term saving product that provides guaranteed returns and tax benefits. One of the advantages of this saving scheme is that it allows you to keep your investments secure while generating interest at competitive rates (7.1% per annum).

The scheme had two distinct objectives behind the features and benefits it offered:

- Provide a retirement savings option to unorganised sector employees and self-employed Indians

- Offer a flexible yet long-term investment option for the general public

PPF combines and caters to both the goals with sovereign guarantee and tax benefits of the scheme.

Public Provident Fund Scheme (PPF) is a long-term savings scheme with good interest rates and guaranteed returns. One of the most incredible things about PPF is that the returns and interest gained through PPF are tax-free.

The scheme offers flexibility and partial withdrawal facilities to support you financially during the long investment tenure. PPF Account balance is also free from attachments under court orders.

Thus, it makes sense to invest in PPF for the self-employed, as a PPF account will ensure financial stability for the family.

| Interest Rate | 7.1% PA (from April 2020) |

| Minimum Investment Needed | Rs 500 |

| Maximum Investment Limit | Rs. 1.5 Lakh PA |

| Tax Benefit | Up to Rs. 1.5 Lakhs under section 80C |

| Tenure | 15 Years (Which can be renewed in blocks of 5 years) |

| Risk Profile | Very Safe. Offers sovereign guarantee on capital and interest |

| Maturity Amount | Depends on the Tenure of the Investment |

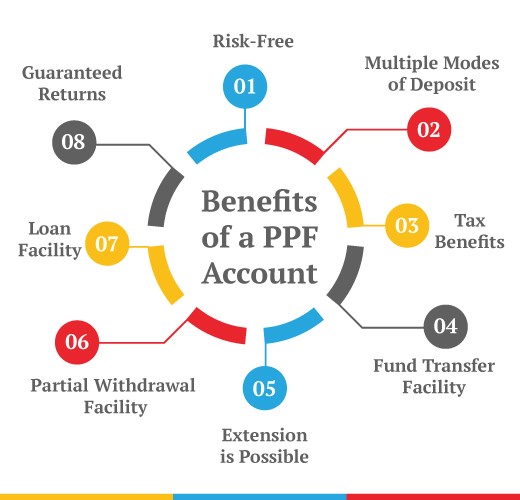

Public Provident Fund can provide you with many benefits. It’s crucial to understand what is PPF and how important the PPF is and to do that, we will show you the benefits of the PPF scheme.

PPF Scheme is the best option if you are looking for a long-term investment with guaranteed returns. With a very minute effort, you get the tax-saving tool, guaranteed returns, and centralized rates. This is why investing in PPF can be the best thing you can do.

The PPF interest rates are fixed at 7.1% for the third quarter of FY 2022-2023, meaning the 1st of October 2022 to the 31st of December 2022. The interest amount is calculated based on your lowest balance each month. The lowest balance is considered between the 5th and last day of the month. That’s why, if you are investing in PPF, make contributions before the 5th day of the month.

PPF scheme is a long-term investment and has no maximum maturity age. The initial holding period of the PPF scheme is 15 years. You can further extend this period in blocks of 5 years. So, you can continue your PPF account for a lifetime after it matures.

The minimum and maximum limits to investment are set in PPF. However, this bracket is broad enough for any investor. The minimum amount that you can invest in PPF is Rs 500 pa and the maximum amount is Rs. 1.5 lakhs pa.

Once you start investing in a PPF account, you can invest any amount within the given investment limits in the account. You do not have an obligation to invest a fixed sum every month or year. However, it’s better to maintain a disciplined investment streak.

As we have mentioned earlier in the article, the returns you gain from Public Provident Fund are completely tax-free. You don’t have to pay taxes on the money you earn through the interest on your PPF investment. This can help you as a tax-saving tool.

You can take a loan against your PPF account balance. The only condition is that you can take this loan after 1 year of starting a PPF account and before the expiry of 5 years.

The amount of loan that you can take is 25% of your PPF balance at the end of the second year. Otherwise, the balance of the year preceding the year in which you applied for the loan is considered.

You can open a PPF account at any time you want in a year. It is best to invest in this fund as it will offer a better power of compounding over the years. The account can be extended for five years multiple times after maturity. Take care of the following while starting your PPF investments:

You can get the required forms from any bank which is authorized for PPF account opening.

The Ministry of Finance declares PPF interest rates every quarter. These interest rates are now set every quarter based on market conditions. This was implemented in the financial year 2017-2018. Let’s take a look at the quarterly interest rates since 2019.

PPF interest rates for the year 2019 were as given below:

In the year 2020, the quarterly PPF interest rates were as follows:

Since the year 2020, the PPF interest rates have been 7.10% only and at present, it’s still the same. This interest rate is not dependent on any market. Instead, it’s set by the Central Government itself.

Now that you know what PPF is, you must know how to start your Public Provident Fund account:

Your PPF account is now open and all set. Apart from the online process, you can open your PPF account via a bank branch or Post Office as well.

For opening a PPF account offline you will need to fill out the appropriate account opening form and submit signed copies of all KYC documents.

Public Provident Fund Account has a holding period of 15 years. However, you can withdraw a partial amount from your PPF account. The rules are:

You can take up a loan against your PPF balance. However, there are certain conditions and some things you must follow.

You can take a loan against PPF only after the completion of 1 year after opening your Public Provident Fund Scheme account and before the expiry of 5 years after opening a PPF account. That’s the time window in which you can apply for a loan against PPF.

You must submit Form-D. This form asks for details like account number, loan amount, etc. The form also needs you to affirm that the loan will be paid back with interest within 3 years.

You can only take a loan for the amount of up to 25% of the account balance at the end of the 2nd financial year of your PPF account or the year proceeding the year in which you applied for the loan.

If you repay the loan within 3 years, the interest rate of 1% p.a. will be applied. However, the interest rate of 6% is applied if you do not repay the loan within 3 years.

You don’t pay the interest rate with the EMIs. You only repay the principal amount through your EMIs. After the principal amount is repaid, you have to pay the interest amount within the next two months.

You can close your Public Provident Fund account only after completing the initial tenure of 15 years. To close your account, follow these steps:

After you close your PPF account, your payment will be deposited in the savings account that you have linked with your PPF account.

An individual can withdraw money from PPF after it has been in the account for a minimum of 5 years. There is no specific duration for this. You can withdraw anytime you want as long as you have waited for at least five years from the account opening date.

The withdrawal amount cannot exceed 50% of the total amount in your account or a maximum limit decided by the government every year.

Your account will be considered inactive if you don’t deposit at least Rs 500 in your Public Provident Fund account in the year. You can retrieve your inactive PPF account.

After the completion of the first 15 full financial years, your PPF account is ready for maturity and full withdrawal. After this, you can either choose to extend your PPF account with or without contributions in blocks of 5 years.

If you don’t take any action after maturity, your account will be continued without any need for further contribution. You can choose to extend the tenure up to 5 years with an annual contribution if you want to invest more in PPF.

To extend your PPF account with contribution, you need to fill out Form-H with a request to extend the tenure.

| Equity Linked Saving Scheme (ELSS) | - Pure equity diversified mutual fund - Offers tax benefits under section 80C - Minimum lock-in of 3 years for each investment - No limit on investment, minimum investment can start from Rs 1000 |

| Unit Liked Insurance Plans (ULIPs) | - Made for serving any long-term goal - Invest in a flexible portfolio of equity and debt funds - Best for meeting important life goals of children or family members - Offers a life cover and protection for investment - Bonus additions for long-term disciplined investors - Minimum lock-in of five years - The maximum tenure of up to 99 years of age |

| National Pension Scheme (NPS) | - Made for serving retirement saving goal - Allows investment in managed portfolios of equity, debt (corporate and Gilt) and alternative assets - Full withdrawals are allowed only after 60 or superannuation - Tax benefits of up to Rs 2 lakh per year - Your employer can also contribute to your account |

| National Saving Certificate (NSC) | - A flexible investment scheme with a sovereign guarantee and a good rate of interest - The maturity period is five years - Tax benefits under section 80C |

| Sukanya Samdriddhi Yojana | - Great scheme if you have a daughter - Tax benefits under section 80C + tax-free interest - The fund value vests to your daughter as she attains 21 years of age - Offers protection from the attachment under court orders |

ULIPs and NPS accounts have been a fair competition for PPF accounts. However, PPF has been the most popular scheme due to its flexibility. We highly recommend PPF over other options available.

As per the recent amendments in PPF account rules, you cannot have more than one PPF account. If you had more than one PPF account in your name both accounts will be merged into one. You can choose which account to continue after the merger.

Yes. You can write a request to reactivate your Public Provident Fund Scheme account with the bank. The fine for the inactivity of the account will be Rs. 50 per year for all inactive years. Along with that, you have to deposit a minimum of Rs. 500 for all the years in which your account has been inactive.

The minimum lock-in period in the PPF scheme is 15 years. This tenure can be extended in blocks of 5 years after reaching maturity.

No. You can choose to extend the tenure in blocks of 5 years with further contribution. Or you can choose to extend the PPF account without further contribution.

There’s no limit to that. You can extend your PPF account tenure as many times as you want. However, you can only extend it in blocks of 5 years at a time.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.