Written by : Knowledge Centre Team

2022-09-26

871 Views

Share

Public Provident Fund or PPF was introduced in 1968, as a means to provide everyone equal opportunity to save for their retirement. The 15-year saving scheme was to bring the self-employed and unorganised sector employees to par with the organised sector workers.

This investment option has evolved significantly over the years and today serves as one of the best sources of long-term savings and tax benefits. In this article, we will discuss what is PPF scheme and highlight its features and tax benefits.

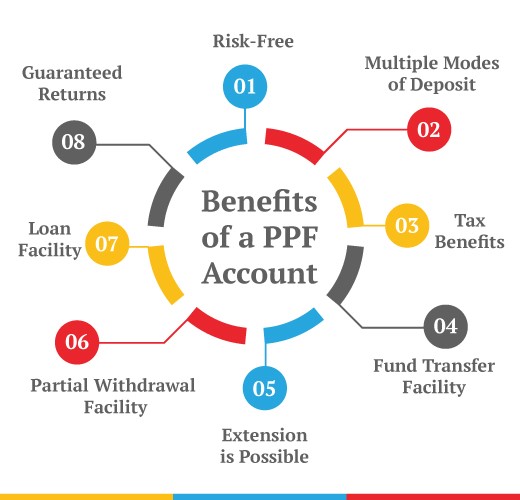

Public Provident Fund (PPF) is a long-term saving product that provides guaranteed returns and tax benefits. One great advantage of this scheme is that it allows you to keep your investments secure while generating interest at competitive rates (7.1% per annum).

Funds in a PPF account are protected against all contingencies, including bankruptcy or loss of job during tenure. As such, it is one of the safest investment options for individuals with a low-risk appetite.

PPF account has kept up with the changing market situations and is one of the most popular retirement related investments. The following features of the PPF account make it one of the must-have investments in India:

You can open a PPF account at any time you want in a year. It is best to invest in this fund as it will offer a better power of compounding over the years. The account can be extended for five years multiple times after maturity. Take care of the following while starting your PPF investments:

Recommended Reading - Compound Interest Investment

Creating your tax-free pension after you turn 60 is easy with PPF if you start investing in the plan early, i.e. before or by 30 years of age.

Assuming you invest Rs 8500 per month in PPF and earn an average return of 7% per annum, at the age of 60, you will have approximately Rs 1 crore in your PPF account.

Using the partial withdrawal facility, you can withdraw an average income of Rs 68,000 per month from the deposit up to the age of 90.

While the total annual income amounts to more than Rs 8 lakhs, this entire amount is free from any direct or indirect tax liability.

You can open a PPF account at a post office or any centralised bank either offline through a branch or online banking.

An individual can withdraw money from PPF after it has been in the account for a minimum of 5 years. There is no specific duration for this. You can withdraw anytime you want as long as you have waited for at least five years from the account opening date.

The withdrawal amount cannot exceed 50% of the total amount in your account or a maximum limit decided by the government every year.

Withdrawal Process

1. Download Form C from your bank's/post office website. Fill in the relevant details.

2. Submit the form to the bank/post office branch where you have your PPF account.

Form C consists of the following three sections:

Section 1: The declaration section wherein you need to provide details such as your PPF account number and the amount you wish to withdraw. Along with that, you also have to specify how many years have passed since you opened the PPF account.

Section 2: The Office Use Section which comprises details such as:

Section 3: The bank details section, asks for your bank details such as your bank account number, IFSC code, etc.

Two investments which are comparable to PPF and even better for aggressive investors are as follows:

NPS is a government-sponsored pension scheme for retirement savings in India. It is regulated and governed by PFRDA (Pension Fund Regulatory and Development Authority).

An NPS Account offers the following benefits:

Also Visit - How to Invest in NPS?

A ULIP is a life insurance plan which allows investment into diversified market portfolios of equity and debt. When you buy a ULIP, part of the premiums goes towards your life insurance, and the rest is invested in the fund of your choice.

iSelect Guaranteed Future is a guaranteed plan with an option to receive income once you turn 60. The plan is also comparable to PPF in terms of safety of invested capital and interest earned:

PPF is a low-risk investment option that provides people with a decent tax-free return. It is also an effective retirement saving tool for those who do not want to invest in equities. The returns are comparatively low but steady and predictable, which makes it a great long-term investment plan for both new and experienced investors.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.