Locate branch

Resume journey

Pay Premium

Contact us

Does the thought of retirement cross your mind sometimes? Do you have enough wealth to manage your monthly expenses if you decide to retire? You may not have it, but you can start preparing for it.

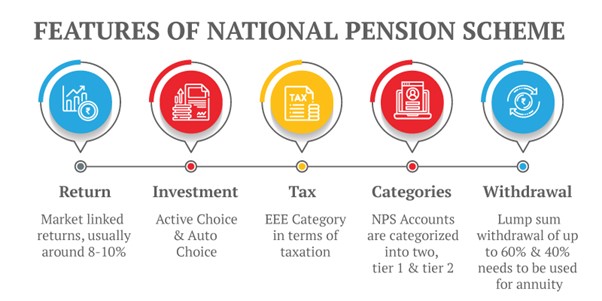

You must build a corpus that will aid your financial requirements post-retirement. And if that's on your mind, the National Pension System (NPS) can be your ideal pick. NPS is a Government of India-backed financial tool that allows you to spend your money across various asset classes to build your perfect retirement corpus.

Types of Accounts in the National Pension System

NPS is governed by the Pension Fund Regulatory and Development Authority of India (PFRDA). If you are 18 to 65 years old, you are eligible to invest in the NPS. In recent times, the NPS rules have been flexible to adapt to the evolving times, thus making this saving scheme investor friendly.

NPS offers the following two types of accounts:

1. Tier I NPS Account

Tier I is a retirement account. On opening a Tier I NPS account, you are allotted a 12-digit permanent retirement account number (PRAN). You can open this account with a minimum contribution of Rs 500. However, to keep the account active, you need to contribute at least Rs 1,000 in a financial year.

There is no cap on the maximum investment you can make to your Tier I account. The money you invest in this account is locked until you turn 60. On turning 60, you can withdraw 60% of the corpus as a lump sum. You must use the balance of 40% of the corpus to buy an annuity plan from an insurance company that will pay you a monthly pension.

Under Section 80CCD of the Income Tax Act 1961, the investments you make to your Tier I NPS account qualify for tax exemption.

2. Tier II NPS Account

Tier II accounts are permitted only if you already have a Tier I account. This voluntary account can be opened by making a minimum deposit of Rs 1,000. Later, you can contribute any amount that you wish to.

One significant factor differentiating Tier II accounts is that the investments made in Tier II accounts do not enjoy any exemption. You do not get any benefits from your Tier II account investments.

Recommended Reading - NPS Returns

How to Open an NPS Account?

You can open your NPS account both online as well as offline following the processes and documents given below:

Follow the below steps to open your NPS account online

1. Visit the official NPS website. Click on the 'Registration' tab and select 'Individual.'

2. Fill in your Aadhaar card and PAN card number. On doing so, you will receive a one-time password (OTP) on your registered mobile number.

3. Enter the OTP and click on the 'Continue' button. An acknowledgement will be sent on the number with your name. Click on 'OK.'

4. You will be redirected to a new page. Fill in your details and then click 'Save and Proceed.' Next, you are required to select your asset allocation - Auto or Active. After you have chosen the option, fill in the nominee details.

5. Post that, upload a cancelled cheque from your bank account and your specimen signature.

6. Lastly, you need to pay a minimum of INR 500. On making a successful payment via net banking, you will receive your PRAN number and the payment receipt.

Opening an NPS Account Offline

1. Visit your nearest point of presence (POP), appointed by the PFRDA, with the photocopies of the original know-your-customer (KYC) documents. Almost all banks are enrolled as POPs. Also, keep the originals handy for verification purposes.

2. You will be given an application form that you must fill with a black pen.

3. After filling up the application form, you will receive a 17-digit receipt number.

4. On successful verification of your application, a kit containing your PRAN number will be delivered to your registered address.

5. You will also receive a message or an SMS on your registered mobile number informing you about your PRAN number and the kit dispatch.

Documents Needed to Open NPS Account

- Aadhaar Card

- Net-banking details

- Passport size photographs

- Scanned image of your signature

- PAN Card

Selecting your Ideal Portfolio in NPS

1. Active Choice (Individual funds)

You can actively decide how your contribution will be invested in an active choice option. You are required to provide the PFM, Asset Class, and percentage allocation to be done in each scheme. There are the following four Asset Classes that one can choose from:

- Asset class E: Equity

- Asset class C: Corporate debt

- Asset class G: Government Bonds

- Asset class A: Alternative Investment Funds

2. Auto Choice (Lifecycle funds)

This option is for those who do not have adequate knowledge to manage their investments. Under this option, a pre-defined portfolio will decide the proportion of funds invested across three asset classes.

Based on the risk-taking ability of the Subscriber, NPS offers three different portfolio options with age-wise percentage asset allocation as follows:

a. Aggressive Life Cycle Fund (LC75):

Aggressive Life cycle fund comes with a cap of 75% of the total assets for Equity investment.

| Age | Asset Class E | Asset Class C | Asset Class G |

|---|---|---|---|

| Up to 35 years | 75 | 10 | 15 |

| 40 years | 55 | 15 | 30 |

| 45 years | 35 | 20 | 45 |

| 50 years | 20 | 20 | 60 |

| 55 years & above | 15 | 10 | 75 |

b. Moderate Life Cycle Fund (LC50):

Moderate Life cycle fund has a cap of 50% of the total assets for Equity investment.

| Age | Asset Class E | Asset Class C | Asset Class G |

|---|---|---|---|

| Up to 35 years | 50 | 30 | 20 |

| 40 years | 40 | 25 | 35 |

| 45 years | 30 | 20 | 50 |

| 50 years | 20 | 15 | 65 |

| 55 years & above | 10 | 10 | 80 |

c. Conservative Life Cycle Fund (LC25):

This Life cycle fund offers a cap of 25% of the total assets for Equity investment.

| Age | Asset Class E | Asset Class C | Asset Class G |

|---|---|---|---|

| Up to 35 years | 25 | 45 | 30 |

| 40 years | 20 | 35 | 45 |

| 45 years | 15 | 25 | 60 |

| 50 years | 10 | 15 | 75 |

| 55 years & above | 5 | 5 | 90 |

Tax Benefits of Investing in NPS

All individual subscribers get tax benefits under Sec 80 CCD (1) with an overall ceiling of INR 1.5 Lakh under Sec 80 CCE. An additional deduction for investment up to INR 50,000 in NPS Tier I account is also available to NPS subscribers under subsection 80CCD (1B).

This deduction is over and above the deduction of Rs. 1.5 lakh under section 80C of the Income Tax Act, 1961.

Also Read - How to Withdraw Pension Contribution?

Alternatives to NPS

There are few investment options in India which can beat NPS as a long-term retirement saving plan. However, you can consider unit-linked insurance plans (ULIPs) like Invest 4G from Canara HSBC Life Insurance for the goal:

- Invest up to the age of 99 years after starting any time after 18 years of age

- Invest in a mix of equity and debt funds

- Investments up to Rs 2.5 lakhs per annum in ULIPs will keep your plans’ maturity values tax-free

- Automatic rebalancing options keep your folio benefiting from market volatility

- Bonus additions for long-term investors aid your folio growth

- Life cover improves the safety of your family in your absence

- Partial withdrawals are tax-free and available after five years of starting the plan

Must Read - Is Pension Taxable?

Click here - NPS Withdrawal

NPS can be your ideal solution if you want a savings scheme to support your retirement. The options and benefits of the NPS make it the most preferred choice. However, diversification to ULIPs can help you maintain liquidity as well as growth.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

894 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

871 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

875 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan