Locate branch

Resume journey

Pay Premium

Contact us

Want to do better for your retirement without becoming a retirement planning expert? Lean on the simple and basic concepts of retirement savings. And before we dive into these amazing concepts let’s recall a few old age wisdom nuggets which hold even in modern times:

- Plan for the worst & hope for the best

- Save first, spend later

- Time is the greatest factor in the growth of your wealth

Retirement is ultimately just another financial goal and like any other financial goal, it depends on the simple mathematics of expenses and savings. You need to manage your expenses and increase your savings to achieve more with your income.

Thus, following these principles, while planning we will stay realistically conservative. Also, these principles will be corroborated by the retirement concept again and again as you will see.

THE CONCEPTS:

1. Early Retirement means Longer Distribution Period

Retirement goal is not a static goal situated at one point in time. It is a continuous goal, which begins the moment you start earning and continues till you live. The whole retirement journey is divided into two phases

- Accumulation phase, when you save, invest and try to accumulate a huge corpus

- Distribution phase, when you stop investing and expect the corpus to support you financially for the rest of your life

Nowadays, ‘early retirement’ had been quite a buzzword among Gen-Y. However, what does early retirement mean?

If it means for you to hang your boots and start living your money, you will soon find it difficult for the following reasons:

- Early retirement means, your money gets less time to grow; i.e. lower money pool

- Your distribution period will be longer; i.e. the smaller corpus must last longer

- Inflation will be more prominent for you; inflation is higher in younger years as lifestyle builds up

Thus, early retirement should mean that you will start working on something closer to your heart. Starting a business enterprise and making it profitable has been one of the popular early retirement plans.

2. Inflation vs. Pension

You should expect that inflation will affect your expenses, even after retirement. However, as your lifestyle expenses slowdown in the later years, inflation will have negligible effect. But in the early years, the effect of inflation is much higher.

Thus, the chance of your corpus depleting much faster than you expect is higher in the early years. So, while investing for your retirement goal, you need to ensure that you can accumulate more than your estimate. This will need you to:

- Use high-risk-high-reward investment options, such as equity funds

- Manage your portfolio risk so that your corpus keeps growing

- Use plans which will do both of the above automatically for you, few examples are, Tier-I account of New Pension Scheme, pension plans from life insurers, online ULIP plans

Best online ULIP plans have the features to allow you to not only invest in good equity funds but also, manage your portfolio with proven strategies. ULIPs like Invest 4G from Canara HSBC Life can easily double up as your tax-free retirement plan in India.

3. Make Sure Your Savings Grow with Your Income

When you plan your retirement, you are planning as per your current income and expenses. But, both will likely change over time, and if stars are properly aligned, income will grow more than the expenses. Your retirement savings should grow along with your income, and if possible more than the income growth.

For example, you receive an increment of 10% on your annual income. First thing you need to do, before going out on the party, is to increase all your investments by at least 10%.

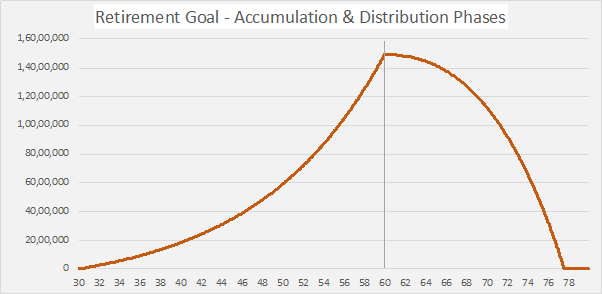

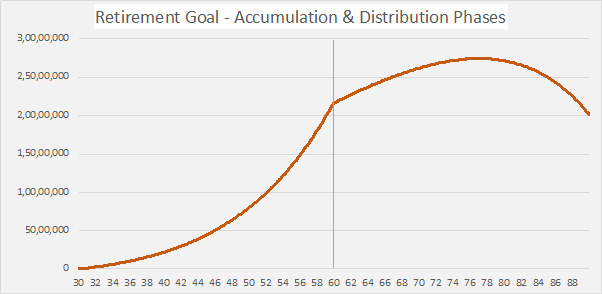

In the first chart of accumulation and distribution phase, we kept investing the same Rs. 10,000 every month for the entire period. The result was the corpus did not even last for the next 20 years.

However, if you increase your savings by just Rs. 500 a month each year, you get enough corpus to last more than 30 years. Not only that, but you can also leave a significant legacy for your children.

Withdrawals are same in both the estimates and growing at the same rate each year.

4. Savings Ratio vs. Time to Retirement

This is one of the most interesting concepts of retirement planning. This concept gives a simple connection between your savings ratio for retirement goal and your ability to replicate the same income.

For example, if you are earning Rs. 1 lakh a month, and save 10% of your income towards retirement, you can replicate the same income within 30 years.

Similarly, Image 3 gives you more years to retirement based on other savings ratios. Rate of return of the investment plays a role in these estimates, and we have assumed 8% p.a. ROI for our calculation.

You have known that ‘the more you save the faster you will achieve your financial goal,’ but this image should solidify your knowledge into firm belief with numbers.

PS, if you save 90% of your income, you can have enough money to replicate the same within the next 10 years.

5. Minimizing Post-Retirement Expenses

While we have been trying to maximize our savings and returns so far we should not miss the beat on expenses. Growing expenses can easily outmanoeuvre your income growth and even most meticulously laid out plans. So, what you do?

You figure out which are the possible major expenses post-retirement and you take measures to minimise them. For now, these could be the most common major expenses on most post-retirement budgeting sheets:

- Medical costs

- Travelling

- Home maintenance/rent

So, taking care of your health will possibly resolve at least two of these. However, you should also keep the senior citizen health insurance handy, just in case the uninvited knocks on your health. For home maintenance, moving to a more manageable property could be recommended. But, there could be so many more solutions.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

893 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

870 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan