Written by : Knowledge Centre Team

2022-10-10

871 Views

Share

What’s better than knowing that you can get money after retirement? Knowing how much money you get after retirement. Defined Benefit Pension Plans are the retirement benefit plans in which you already know how much money you are going to get after retirement.

The return is calculated based on your salary amount and your service period in years.

A defined benefit plan is usually the result of your consistency and discipline rather than your financial contributions. Gratuity and leave salary are the two most popular defined benefit plans available to the employed workforce in India.

Here’s more about the defined benefit plans available in India.

Defined Benefit Plans give you a definite amount based on predefined formula regardless of your actual contribution to such plan. There are formulas to calculate the resultant value and the major factors of that formula are, salary amount and years of service.

Some salient features of defined benefit plans are as given below:

Employers might use some insurance policy to provide you with gratuity. Otherwise, it’s a CTC. That’s because a company must pay gratuity to the employers who have completed certain years of service.

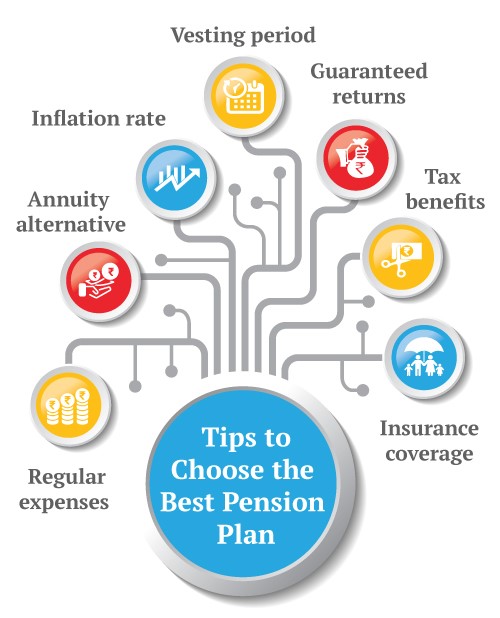

Many Defined Benefit Plans are defined based on years of service. Mostly this period is called the vesting period in a company that offers a Defined Benefit Pension Plan. An employer who leaves the company before the completion of the vesting period may not be entitled to the complete benefits of the Defined Benefit Plan.

Your returns are dependent on which plan you take. Many life insurance policies in India give returns as a lump sum of money. Some might provide a regular sum of the amount.

Most defined benefit plans provide you with the option to decide how they want their funds to be delivered. The following are some of the often-provided payment options:

1. A single-life pension provides a set income each month for as long as the beneficiary lives. No payments are provided to the policyholder's survivors after his or her passing.

2. A lump sum payment is made when one receives the full amount of their plan. When the policyholder passes away, no more payments are provided to the survivors.

3. A Qualified Survivor and Joint Plan: Until death, the insured receives a set monthly benefit. Benefits are also paid to the policyholder's surviving spouse if that person is alive. When a spouse receives pension or retirement benefits, they get at least half of the policyholder's total pay-out.

Making the proper payment choice is important since it may influence how much benefit you ultimately receive. Therefore, you should carefully weigh all the available possibilities and evaluate the benefit amounts offered by each.

Also Read - How to Withdraw Pension Contribution?

Defined benefit plans offer a range of benefits, but there are certain disadvantages to these plans too. Here’s a list of both pros and cons of these plans:

Employee incentives are assured under a set benefit plan, providing retirees with a higher retirement benefit.

Employee retirement benefits remain unchanged regardless of what happens to the markets or investments.

After an employee's passing, a spouse could be allowed to receive the benefits.

Employers may often deduct their payments to defined benefit plans from their taxes.

Employees who participate in defined benefit plans might stay with a firm for a long time as they wait for their benefits to vest and begin to accrue the most.

You will not influence the investments made with their funds.

If an employer needs six years of service before a benefit becomes vested, and you quit after four years, all the funds you have earned will remain with the employer.

Although it may be simpler with cash balance plans, it may be challenging to transfer funds from one plan to another as a person changes employment. This does not imply that you won’t be getting all the collective benefits when you retire. Simply maintain numerous sources of income.

Because the benefits equation is fixed, you cannot grow your retirement income.

Defined benefit plans are more demanding for firms to operate than defined contribution schemes since they provide assured pay outs irrespective of market circumstances.

The Indian retirement system is a mix of defined contribution and defined benefit plans. The following types of defined benefit plans are available in India:

Statutory benefit applicable to employers with 10 or more employees.

Not statutory but helps promote work-life balance among employees and compensates fairly for eligible leaves.

Life insurance benefit is available to the employee’s family in the case of the sudden death of the employee.

Compensates the employee and his/her family in the case of an accidental injury or disability, which may put him/her off the work for a while or permanently.

Click to Visit - Disability Insurance

Provides statutory benefits payable to workers and employees in the case of workplace injury.

Guarantees a minimum monthly pension based on a minimum contribution for a minimum number of years.

Pension plans offered by life insurance companies offer guaranteed lifetime pensions. If held jointly with the spouse, the pension continues until one of the holders is alive.

Click here - Is Pension Taxable?

Statutory defined benefit plans that employers must offer to their employees can be seen as a financial challenge to the enterprises in India. However, you can use the insurance plans to offer these benefits and even offer better benefits than the statutory limits:

Defined benefit plans are a great boost to your retirement kitty. However, do note that your benefits improve with your longevity at your employer. The longer you stick to one employer the better your gratuity and leave salary benefits will be.

Defined benefit plans are almost entirely funded by employers' contributions. But saving schemes and retirement benefits like guaranteed plans will need some contribution from you. However, understanding the plans can help you maximise your benefits from them.

You can earn consistent income even after your retirement. This policy constitutes positively to your post-retirement finances. So, we recommend that you understand the defined benefit pension plans to secure your post-retirement life.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.