Locate branch

Resume journey

Pay Premium

Contact us

Nowadays, retirement is perhaps not possible without a pension plan in place. However, pension plans just don’t appear upon retirement. They are the result of your long-term and continuous efforts during your employed years. These long-term plans are retirement plans and there are two types of them:

- Defined benefit retirement plans

- Defined contribution retirement plans

If you are employed on the salary you likely have access to both types of retirement plans. Discover more about them here.

What is a Defined Benefit Plan?

A defined benefit retirement plan is one where your maturity benefit, or benefit on retirement, has been defined. The benefit will be available to you regardless of your contribution to the plan.

Benefits can be paid in a lump sum or as a regular pension. However, in any case, the benefits are only payable upon your superannuation or relieving.

Examples of defined benefit plans include:

- Leave Salary

- Gratuity

- Voluntary Retirement Scheme (VRS)

- Central Civil Services Pension

- Pension for Public Sector Bank Employees

- Guaranteed Savings Plan

As interest rates decline and markets become more profitable, sustaining defined benefit schemes can become difficult. Thus, over the last few years, many of these schemes have been replaced by defined contribution plans.

What is a Defined Contribution Plan?

Defined contribution plans are retirement plans where your maturity benefit depends on your investments in the plan. The investment or the contribution is usually predefined for you based on your income. The majority of retirement investment plans are defined contribution plans.

Examples of defined contribution retirement plans include:

- Employee Provident Fund (EPF)

- National Pension Scheme (NPS)

- Unit Linked Insurance Plans (ULIPs)

- Voluntary Provident Fund (VPF)

- Public Provident Fund (PPF)

- Life Insurance Pension Plans where pension or maturity benefit is not guaranteed, i.e., unit-linked pension plans

You should always have at least one running defined contribution retirement plan.

These plans give the financial control of your retirement into your hands.

Defined Benefit Vs Defined Contribution Plans

Defined benefit and defined contribution plans have one purpose, i.e., to support your retirement. However, these plans have many differences as well:

| Defined Benefit Plans | Defined Contribution Plans |

|---|---|

| Available only to organised sector employees and government employees | Anyone can avail of these plans including self-employed |

| Only employer contributes to these plans | Both employers and employees can contribute to these plans |

| Unless employer invests in insurance schemes to handle such payments this can affect their liquidity | Employees can avail these plans without employers |

| Benefits depend on the employee’s service tenure and average income | No effect on employer liquidity as the employer is not responsible for benefit payments |

| Employees may not have any control over the benefit amount | Benefits depend on plan performance |

| You can increase/decrease your contribution to change your benefits |

Which are the Best Defined Contribution Plans?

Defined contribution plans are the best retirement savings option for you. The new defined contribution plans allow you to invest as per your risk appetite. Now you can even benefit from long-term equity exposure for your savings.

Here are some of the best-defined contribution plans you can invest in India:

National or New Pension Scheme (NPS)

National Pension Scheme is the new, more versatile form of retirement investment. The scheme is open to corporate and government employees, as well as the public. Here are the salient features of this retirement saving plan:

- Invest a percentage of your income every month

- Employers can also contribute to employees’ NPS accounts

- The account is easily portable from one employer to the other

- Invest in a portfolio of equity, debt (government and corporate) and alternative investment

- Maturity withdrawals available only at the age of 60

- Premature withdrawals are allowed in the case of emergencies

- Lump-sum withdrawal of up to 60% of the total fund value is tax-free at the age of 60. The remaining amount must go into a pension plan.

- No limit on annual investment. However, an employer’s contribution above 10% of salary will become taxable in your hand.

- Tax benefits of up to Rs 2 lakhs on invested money u/s 80C and 80CCD(1B)

Also Read - NPS Returns

Public Provident Fund (PPF)

PPF is one of the most popular defined contribution schemes. The scheme is a government-backed retirement saving plan open for all Indian residents. Salient features of PPF are as follows:

- The rate of return is fixed and carries a sovereign guaranty

- The minimum holding period is 15 years

- You can invest up to Rs 1.5 lakhs every year

- You can withdraw partially after completing 5 financial years

- Within the first five financial years, you can borrow funds from your PPF account

- Invested money and maturity values are exempt from tax

- You can extend the account multiple times for 5 years after completing the 15-year holding period

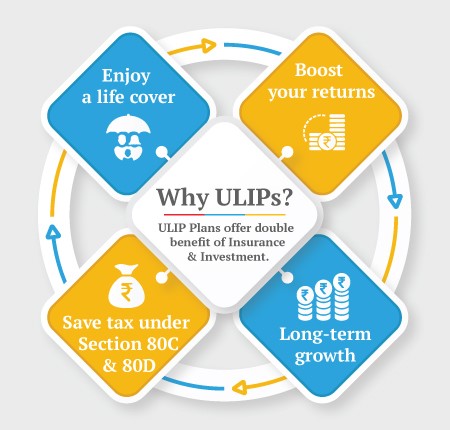

Unit Linked Insurance Plans (ULIPs)

ULIPs are versatile and long-term investment plans from life insurance companies. ULIPs mix the best of both investments and the basic insurance world to provide a flexible and managed investment solution. Here are the salient features of ULIP plans you should consider:

- Invest in a mix of diversified equity, debt, and liquid funds

- You can SIP into equity funds even if you are investing in a lump sum

- You can switch between funds multiple times during the investment period without withdrawing money or paying tax

- Manage your portfolio allocation with automatic strategies

- Investment up to Rs 2.5 lakhs p.a. in ULIPs keep your ULIP maturity and withdrawals tax-free

- ULIPs like Invest 4G from Canara HSBC Life Insurance let you invest in the same plan up to the age of 99 years. Thus, you can build a good corpus till the age of 60 and draw a tax-free pension afterwards from the same plan.

- You can withdraw the fund value partially after five years

- You can avail of an 80C benefit on the invested money

Other than the defined contribution pension plans, you can also avail defined benefit plans from life insurance companies. These are guaranteed pension plans which also provide premium protection features.

You can use these plans to secure the retirement life for your dependent spouse or other family members. The premium protection feature will ensure that the spouse will receive the guaranteed benefit even after your demise within the contribution period.

Financial safety during retirement life depends entirely on your decisions during the employment period. You should invest anywhere between 10 to 30% of your income in defined contributions and guaranteed retirement plans.

Diversifying your investment into guaranteed plans will ensure a minimum safety line for your pension. At the same time, defined contribution plans can replenish your wealth further with market-linked wealth growth.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

893 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

870 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan