Locate branch

Resume journey

Pay Premium

Contact us

Many online life insurance plans nowadays, offer pay-out of death claim as a regular income to nominees. Have you come across such plans and wonder if this feature is anything useful?

Life insurance has been around to ensure financial consistency of the social unit, which is your beloved family. A family which loses its breadwinner can lose its financial status fast, jeopardising the financial future of its younger generation. Thus, life insurance plans, and especially term insurance plans would offer a large sum of money to the bereaved family and help them fulfil their life goals.

Why Income from the Life Insurance Plan?

While, most death claim pay-out will happen as a lump-sum and the nominees would struggle to use the money judiciously. The family would have two financial objectives to achieve out of life insurance proceeds:

- Generate sufficient income every month to continue the household

- Invest in all the important long-term goals like children’s education etc. to ensure a stable financial future for them

To accomplish the first goal the decision-maker would again go back to the insurer and try to secure a pension or annuity plan. There were many reasons to go back to the insurer but the following two have been the most prominent - Life insurance investment can guarantee returns and second, any other safe or fixed income investment would attract more tax liability, in the way of TDS deduction at source, or had limited capacity to accept funds (Post Office MIS).

So, the simple solution where everyone could go home happy was to integrate the income pay-out with the life insurance claim itself. This immediately resolved both the family problems:

- Nominees do not circle back to the insurer for income generation

- Worry about generating a stable long-term income taken care of

- Income is tax-free [u/s 10(10D)] as coming from life insurance proceeds

- Income is guaranteed for the period decided at the time of purchase

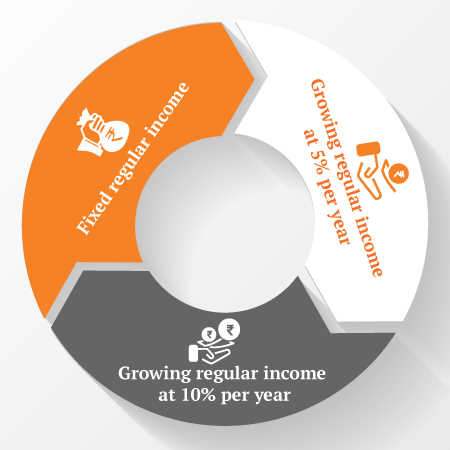

Regular Income Pay-out Options:

Online term insurance plans from Canara HSBC Life, iSelect Smart360 Term Plan, offers very customizable regular income pay-out option. There are three choices available in this plan with the feature

Fixed Regular Income Pay-Out

Fixed regular income pay-out means the income doesn’t change over the years. For example, if the monthly income amount based on your corpus allocation towards regular income is Rs. 50,000 per month; your nominee will receive Rs. 50,000 per month throughout the entire income tenure after a claim.

Explore Regular Income Option under iSelect Guaranteed Future Plus

How’s is it Calculated in iSelect Smart360 Term Plan

The iSelect Smart360 Term Plan uses a multiplier to define the amount of income at the time of claim. See the following example:

- You buy a cover of Rs. 1 crore sum assured (S.A.)

- You distribute this S.A. equally for payment as a lump-sum and regular income; i.e. Rs. 50 lakhs will be allocated for monthly income while the remaining would be paid out as lump-sum.

- The factor for estimating fixed regular income is 10.09 per 1000 of S.A.

- Thus, your nominee will receive Rs. 50 lakh as a lump sum money and Rs. 50,450 a month as regular income (50,450 = 10.9 x 50 lakh / 1000)

Growing Income Pay-Outs

The only difference between fixed and growing income pay-outs is the multiplying factor. The factors for growing income at 5% and 10% are 8.34 and 7.11 respectively. Therefore, your nominee’s monthly income in the first year will be as following:

- At 5% per year growth rate: Rs. 41,700 (will grow by Rs. 2085 every year)

- At 10% per year growth rate: Rs. 35,550 (will growth by Rs. 3555 every year)

You should note that the growth in both the incomes will be at a simple interest rate only.

How Long Does Income Continue?

As much you’d like to think the income doesn’t continue indefinitely. Canara HSBC Life’s iSelect Smart360 Online Term Plan gives you two options to choose from:

- For 120 months

- For 40 years or remaining policy years whichever is lower

So basically, you get to decide how much income your nominee will receive, how much it grows every year and how long will it continue.

How to Select This Feature?

Since the income will only last for a limited time, you can understand that the insurance must also provide retirement corpus for your spouse. Therefore, you should always divide the corpus between regular income and lump-sum amounts.

While regular income is a good addition, it helps to have a large sum of money to invest in your long-term financial goals.

Also, growing income could be a better choice for your family rather than a fixed income for a long time. The simple reason is that lifestyle grows over time, especially over more than 10 years. With the income remaining the same, the family’s lifestyle will have to decline to keep up with the inflation.

However, with income growing at a small percentage the family can take care of the inflation problem. So, make the family’s financial protection a more convenient affair for them with an online life insurance plan with regular income option.

Life Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Recent Blogs

How to Choose the Best Savings Plan in India?

02 Aug '24

890 Views

Read More

Life Insurance

Reasons Why Stay At Home Parents Need Insurance Too

02 Aug '24

873 Views

Work hours extending beyond the standard nine-to-five grind, no provision of leave, juggling work between multiple departments, and no payment-welcome to the life of a stay-at-home parent.

Read More

Life Insurance

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance

02 Aug '24

872 Views

Making Claim Settlement Easy for Your Beneficiaries : Canara HSBC Life Insurance introduces 1 day settlement of death claims, with 98.12% claim settlement ratio

Read More

Life Insurance

Life Insurance The Key to Happiness Post-Retirement

02 Aug '24

870 Views

How does your retirement planning tackles the question of passive income? Can you set yourself free from the need to work after retirement?

Read More

Life Insurance

9 Ways you Can Use Life Insurance in your Life

02 Aug '24

871 Views

Benefits of life insurance span throughout all important stages of your life. Whether it is the financial safety of family or your own retirement uses of life insurance plans are far more than it seems…

Read More

Life Insurance

Popular Searches

- Term Life Insurance

- Whole Life Insurance

- Critical Illness Insurance

- Accidental Death Benefit Rider

- Compare Life Insurance Quotes

- Best Life Insurance Companies In India

- Factors Affecting Life Insurance Premiums

- Insurance For Tax Savings

- Life Insurance For Children

- Life Insurance Rider

- Life Insurance Plans

- Types of Life Insurance

- Term Life Insurance Tax Benefit

- What is Insurance?

- Life Insurance Premium