Written by : Daina Mathew

Reviewed by : Jasmeet Bedi

Jasmeet Bedi

2024-09-27

878 Views

Share

There are uncertainties in life, and even though you cannot mitigate them, you can prepare for them. You are working hard to secure the future of your loved ones. However, in case of your sudden death, all the dreams will remain unfulfilled if you have not planned for them.

The family goes through psychological and emotional losses that cannot be compensated. However, a life insurance policy can compensate for the financial losses to some extent.

There are many kinds of risks involved in life. In simple language, insurance is a risk transfer mechanism. You buy insurance to transfer risk to the insurance company and get the cover for the financial loss you may face due to unexpected events. It is a safety cushion that protects you and your family against contingencies.

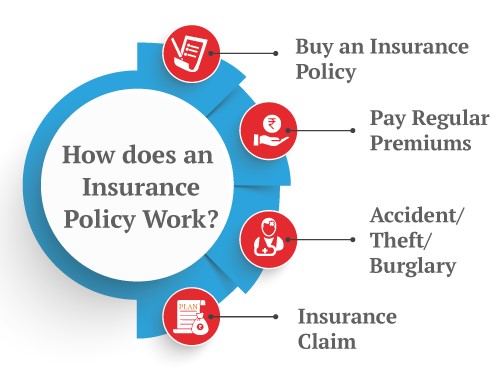

Insurance is a legal contract between you (insured), and the insurance company (insurer) wherein the insurer promises to compensate for financial losses because of unfortunate events like an accident, damage to a house, or untimely demise of the insured.

To understand how insurance works, you should know below terms:

As discussed above, insurance is a legal contract between the insurer and the insured. The insurance policy lists all the policy's conditions and circumstances under which the insurance company is liable to pay you or the nominee the insurance amount.

When you buy an insurance policy from the insurance company, you will have to make regular payments (premium) for a specified period towards the insurance policy.

The insurance company collects the premium from all the clients. They pool the money for losses that may arise out of an insured event. If you don't claim during the policy tenure, you may or may not receive any benefits. It depends on the policy type and the conditions.

You can divide the insurance based on the type of coverage it is providing as below:

It is insurance on your life. You buy life insurance to ensure that your loved ones are financially secured even when you are not around. If you are the only breadwinner, you would want your family members to maintain the same living standards in the event of your untimely demise. The nominee gets the sum assured in case of your death.

Health insurance covers your medical costs for expensive treatments. Different health insurance policies cover different types of diseases and ailments. The premium you pay towards the health insurance policy covers the treatment, medication, and hospitalization costs.

Learn whether you should opt for a long-term or short-term health insurance policy.

These compensate you for the losses sustained arising from a specific financial event that is not related to life. Non-life insurance could be car insurance, home insurance, etc.

You can avail insurance benefits under the following two types of policies:

| Individual Insurance | Group Insurance |

|---|---|

| It caters to an individual and is customized as per one's needs and requirements. | These are insurance companies drawn in the group's name. |

| The premium amount is decided based on your age, family medical history, health, etc. | The premium amount is general and gets deducted from your salary. |

| The premium amount is decided based on your age, family medical history, health, etc. | The group cost is lower. |

Click here to read - Different types of insurance

You must have insurance for the below reasons:

You must know the importance of insurance in your life, and once you understand it, you must have below insurance policies:

This is the purest form of life insurance wherein you pay a premium towards the policy, and in case of your death during the policy tenure, the nominee receives the sum assured. With term insurance, you can receive high coverage against a lower premium. iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers critical illness cover against 40 listed illnesses.

Knowing the rising cost of healthcare and the number of diseases you can have, it is wise to have a financial cushion against health contingencies.

Knowing the rising cost of healthcare and the number of diseases you can have, it is wise to have a financial cushion against health contingencies.

These are mandatory legal requirements in India, and you must have them if you own a two-wheeler or a four-wheeler. It is compulsory to avail of third-party liability motor insurance. However, you can have a comprehensive package to get covered against the various risks of damage with the personal accidental cover.

Your home is exposed to various kinds of risk like theft, damage due to natural calamity, etc. Hence to protect your home against such damages, you must avail of home insurance.

Such insurance plans will help you stay afloat even after a costly mishap or calamity.

Insurance gives your safety and security benefits and also income tax benefits. The benefits are as follows:

However, the maturity benefit is tax-free only if your annual premium for the policy does not exceed 10% of the base life cover in the policy.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.