Locate branch

Resume journey

Pay Premium

Contact us

In a term insurance plan, the life of the policyholder is covered until a specific time. The insurance company provides death benefits to the nominee under the term insurance plan if the policyholder dies within the term period. Financial security and life cover in partial or entire disabilities, critical illnesses, and tax benefits are some common advantages that come with term life insurance.

But in the case of zero liabilities, is it wise to surrender a term insurance plan? For some, it might seem to be the most reasonable option. But it's important to measure the pros and cons of this decision.

Should you surrender the term insurance plan?

Firstly, understand what type of plan you opt for? Pure term insurance plan does not offer a policy surrendering option. In addition, if the policyholder requires no death benefit, then one can go for surrendering the policy.

Terminating the plan can also affect your family in the future, as term insurance plans provide monthly income after the demise of the sole earner.

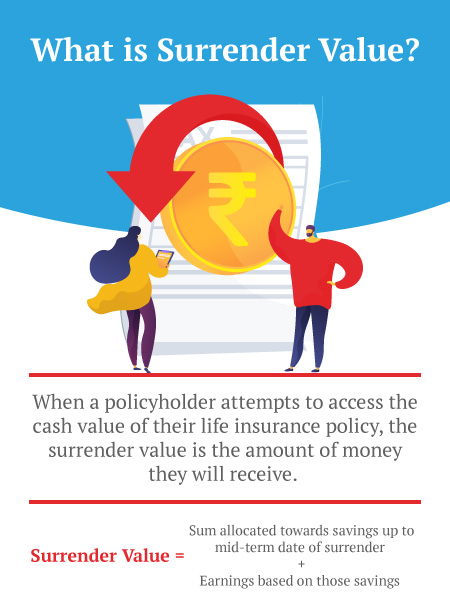

Surrender value

It is an amount the policyholder receives when they voluntarily withdraw from the insurance plan. The insurance company pays some amount to the insured. However, the surrender value varies according to the company's policy term.

According to India's Insurance Regulatory and Development Authority, a surrender value is fixed for the first seven years. This period is the time only after which one can surrender their term plan. Term insurance plans that include savings plans and investment plans and ULIPs are liable to surrender value. Sometimes, the surrender before maturity might also lead to a penalty.

Learn how to calculate the surrender value of life insurance policy.

4 Reasons to avoid surrendering your term insurance

A term insurance plan doesn't only bestow assurance but also several other advantages. It is usually not advisable to voluntarily surrender it. But even if you choose to do it, analyze the consequences beforehand.

1. Effect On future premium

The Premium paid by the insured increases as he/she ages. So, if you surrender a term life insurance policy once, buying another life insurance policy will be expensive. For instance, if a person buys term insurance at the age of 25 and the life cover is one crore for 30 years, then the Premium would be Rs.6,372.

But if the previous policy is terminated and another one is bought at the age of 30 years, then the Premium would increase as much as Rs.7,906. Moreover, if any medical conditions are indicated, later on, your cover might suffer.

2. No return on Premium

Term plans such as iSelect Smart360 Term Plan by Canara HSBC Life Insurance provide an option of return on Premium after the expiry of the policy's tenure. If you surrender the plan, the policy will be terminated immediately, and you can lose this benefit.

3. Tax benefits

The tax benefits that come along with the term insurance plans will be missed out if one decides to withdraw it before the stipulated time as per the prevailing tax laws. Thus, no tax benefits shall be available on a discontinued policy.

4. Protection from medical ailments

Life is uncertain, and term insurance is the way to conserve your financial aspects. The policies are payable in terminal illness so that the unfortunate events don't drain you financially.

Alternatives to surrendering term insurance plan

Now that we have discussed the reasons not to surrender the term insurance, you might need to reconsider your decision. Here are some alternatives that you can go for rather than surrendering your life insurance plan.

1. Buy iSelect iSelect Smart360 Term Plan

iSelect Smart360 Term Plan is the way to go if you want to cover all the additional benefits and secure your family's financial future. It is a highly flexible plan and caters to the insured person's needs at all walks of life. Some basic features of the policy include:

A. Add your spouse in the same plan.

B. Multiple options for limited cover periods of 5-10 years and the payment option during the working years.

C. Options to increase the life cover on different life stages and requirements.

D. The insurance includes components such as Plan Option Life, Plan Option Life with Return of Premium, and Plan Option Life Plus.

The term policies provided in this plan include the full return of the Premium you pay within the policy term when the tenure ends. It means that if any ailment or deaths occurs before the maturity period, the total Premium paid will be repaid, thus terminating the term insurance plan. In addition, an Extended Cover Period can also be added to continue the plan post-maturity.

2. Reduce the term insurance plan

If you do not want to overburden yourself with repeated premiums, then this is a good option. In such plans, the cover amount reduces as the term maturity period comes near. It consists of lower premiums as compared to the other term policies.

Therefore, when you surrender a term life insurance policy, you lose the policy coverage. Also, the key motive of the term plans is to assist the dependants after the unforeseen death events. So, it is basically for the family's safeguarding. It is advisable to balance and think about the repercussions before surrendering your term plans.

The term insurance plans with additional benefits provided by the Canara HSBC Life Insurance come with affordable prices for life covers and benefit pay-outs to serve your needs.

Term Insurance - Top Selling Plans

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Family Shield: Enhanced Protection

- Affordable prices

- Multiple premium payment option

- Get Tax benefits

- Hassle-free purchase process

Recent Blogs

Why Is Medical Test Important In Term Insurance?

02 Aug '24

875 Views

Medical tests are a crucial component of your term insurance buying journey. Read to know more about the importance of these medical tests for term insurance.

Read More

Term Insurance

Why Is It Important To Check Your Term Insurance Premium?

02 Aug '24

876 Views

It is important to understand your premium, as this amount defines the coverage and benefits you will enjoy during or after your policy term.

Read More

Term Insurance

Why Online & Offline Term Plans Differ on Premiums?

02 Aug '24

881 Views

Online term plans are cheaper vis-a-vis offline plans because of the economics of business involved. It is also hassle-free and convenient.

Read More

Term Insurance

What Is The Concept of Joint Term Insurance?

02 Aug '24

876 Views

In contrast to an individual term plan, a joint term plan covers two people in the same policy and offers several benefits for both partners. Joint plans offer unique benefits for both partners that can prove to be vital to meet long-term goals.

Read More

Term Insurance

why should You Renew Your Term Insurance Policy

02 Aug '24

871 Views

There are three broad kinds of insurance policies- term insurance, whole life insurance, and endowment policies. A whole life policy is one in which you pay premium till the death of the insured.

Read More

Term Insurance

Popular Searches

- Types of Term Insurance

- iSelect Smart360 Term Plan

- Term Insurance Plan

- 1 Crore Term Insurance

- 2 Crore Term Insurance

- 5 Crore Term Insurance

- Single Premium Term Plan

- Term Insurance Calculator

- Canara HSBC Life Insurance Young Term Plan

- Term Insurance Tax Benefit

- Term Life Insurance Vs Life Insurance

- Term Insurance For 50 Lakhs

- Zero Cost Term Insurance