Locate branch

Resume journey

Pay Premium

Contact us

Mortality Protection Gap or MPG is a data that is released by the world’s largest re-insurer, Swiss-Re every year. MPG shows the gap between the required financial protection and present life cover of the people in a country.

According to the latest data (2020), Indian people have the largest MPG of about 83%. This means if they need a term insurance plan of Rs. 100, they only have about Rs. 17 as the sum assured in their term insurance plans.

Single Income Families & Personal Priorities

With such overall statistics, when it comes to women in the country, their participation is even lower whether earning or not. Now one of the big reasons is that India is still dominated by single-income families.

Thus, the life insurance majorly concerns the male member of the family who is earning. Does this mean that women in double-income families are buying adequate term insurance?

Probably not, as the Swiss-Re study points out. Even when women are the breadwinner in the family they tend to prioritise health over life. So, either they do not feel the need to buy term insurance or get a small life cover plan.

Even after buying many discontinue the policy after a few years considering term insurance cover to be unimportant.

Financial Value of Homemakers

There cannot be a greater myth than that the homemaker does not have financial value for the family. Although it is difficult to estimate the value, it’s not impossible.

Estimating the economic value of a homemaker without a formal income needs the replacement method of calculation.

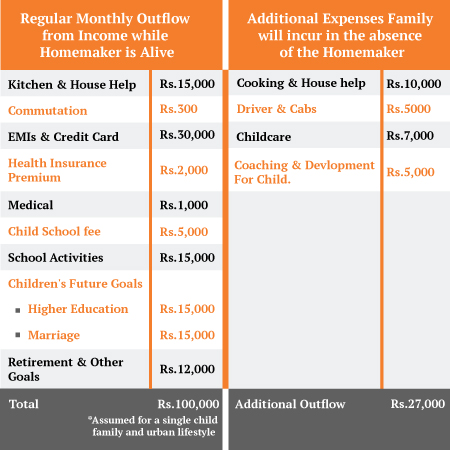

For example, homemakers contribute to the family and children’s welfare, and in their absence all of it must be replaced. But most of these replacement services will cost money:

If your family’s monthly budget looks something similar to the table above, you can see the impact of the additional outflow. You will need to adjust that extra Rs. 27,000 within your monthly budget.

This will directly impact your investments towards your children’s and your own financial goals. Unless the homemaker also has a term insurance plan with adequate life cover.

How Much Life Cover Would You Need?

For Homemakers

Using the replacement method above, the family will need Rs. 27,000 every month to continue their lives without affecting their financial status. To generate Rs. 27,000 every month from a lumpsum investment in a low-risk asset the family will need about Rs. 51 Lakh (Estimated at 6% p.a. for a period of 50 years).

For Earning Women & Primary Breadwinners

If you are earning money from formal employment or business, estimating your economic value becomes easier. You can simply aim to replace your income for the family.

For example, if you are earning Rs. 100,000 a month, you should buy term insurance of approximately Rs. 2 crores.

You may find the premium slightly high for this term insurance cover. But, in any case, you should have a life cover which is at least 10 times your annual take-home income; i.e. Rs. 1.2 Crore in the example above.

Is Term Insurance Sufficient?

Term insurance or life cover is important but definitely not sufficient financial protection for your family. You should always consider additional benefits or riders with the term insurance plan.

You can buy riders like personal accident and critical illness cover with your term cover and enhance your family’s financial safety.

- Personal Accident Cover: Supports the family in case of accidental death and disabilities. PA insurance covers both temporary and permanent disabilities.

- Critical Illness Insurance: CI cover provides financial support to you in case you are diagnosed with one of the life-threatening diseases like heart attack, cancer, renal failure etc.

Anything Else You Should Take Care Of?

You can use certain features offered by the term insurance plans, for instance the iSelect Smart360 Term Plan, to ensure a financially less stressful time for your family:

- Regular Income Pay Out: You can choose this option and set aside a part of the sum assured to be paid as monthly income. This way your family doesn’t have to worry about investing a large sum of money to get a safe income every month.

- Whole Life Cover: If you opt for a whole life term cover, the life cover continues till the age of 99. Meaning even natural death is covered and your children or grandchildren can receive the insurance proceeds as an estate.

- Joint Life Cover: You and your spouse can hold a single policy which will work for both of you. This policy will work the same way as two separate policies would, but will reduce the paperwork and premiums to some extent.

Is Term Insurance Expensive?

Not really. This is the most promising feature of a term insurance cover, especially when you are younger. For example, Rs. 1 crore term plan will cost about Rs. 5500 a year if you are 30 years old female. If you choose to pay this premium every month, you will not even feel its presence (i.e. Rs. 500 p.m.) in your monthly budget.

Single-Premium Option

In fact, if you feel that a commitment of the next 30 years for premium is too much, you can even choose to pay the entire premium in one instance. You pay a little over Rs. 1 lakh for a life cover of Rs. 1 crore, which continues till you are 60.

Do you see any more reasons to not have adequate financial protection for your family?

Term Insurance - Top Selling Plans

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Family Shield: Enhanced Protection

- Affordable prices

- Multiple premium payment option

- Get Tax benefits

- Hassle-free purchase process

Recent Blogs

Why Is Medical Test Important In Term Insurance?

02 Aug '24

875 Views

Medical tests are a crucial component of your term insurance buying journey. Read to know more about the importance of these medical tests for term insurance.

Read More

Term Insurance

Why Is It Important To Check Your Term Insurance Premium?

02 Aug '24

876 Views

It is important to understand your premium, as this amount defines the coverage and benefits you will enjoy during or after your policy term.

Read More

Term Insurance

Why Online & Offline Term Plans Differ on Premiums?

02 Aug '24

881 Views

Online term plans are cheaper vis-a-vis offline plans because of the economics of business involved. It is also hassle-free and convenient.

Read More

Term Insurance

What Is The Concept of Joint Term Insurance?

02 Aug '24

876 Views

In contrast to an individual term plan, a joint term plan covers two people in the same policy and offers several benefits for both partners. Joint plans offer unique benefits for both partners that can prove to be vital to meet long-term goals.

Read More

Term Insurance

why should You Renew Your Term Insurance Policy

02 Aug '24

871 Views

There are three broad kinds of insurance policies- term insurance, whole life insurance, and endowment policies. A whole life policy is one in which you pay premium till the death of the insured.

Read More

Term Insurance

Popular Searches

- Types of Term Insurance

- iSelect Smart360 Term Plan

- Term Insurance Plan

- 1 Crore Term Insurance

- 2 Crore Term Insurance

- 5 Crore Term Insurance

- Single Premium Term Plan

- Term Insurance Calculator

- Canara HSBC Life Insurance Young Term Plan

- Term Insurance Tax Benefit

- Term Life Insurance Vs Life Insurance

- Term Insurance For 50 Lakhs

- Zero Cost Term Insurance