Written by : Knowledge Centre Team

2021-05-24

879 Views

Share

You need all the control over your life you can get, once you hang your hat from work. Ideal retirement is that one event in life that lets you be yourself after you decide not to work. To have such a retirement, your investments play the most significant role. Smart investors consider buying the best retirement plans to fund their retirement dreams. Some other investors also consider putting their money in a mix of assets to enjoy significant returns. While some other consider playing it safe by parking their money in government schemes. So, where can you invest your money for a great and comfortable retired life?

Here are five investments you should have in your retirement investment portfolio:

Guaranteed investment plans are some of the safest long-term investment plans in the country. If you want to preserve your financial wealth for a long time against both inflation and taxes these are the plans you should look for.

Here are two guaranteed investment plans from Canara HSBC Life Insurance for you:

A Guaranteed Savings Plan is a safer alternative for growing your money for a comfortable retirement. As the name suggests the maturity proceeds from this plan is guaranteed. Thus, this is a perfect plan if you need to offer a secure retirement to your spouse in case anything happens to you.

While the plan allows for a tax-free maturity value, it also allows for better growth for a long-term investor. The following bonus additions reward you for staying invested over a long period:

This plan plays an important role in ensuring financial input at retirement. Just in case your other efforts do not bear expected fruits.

Guaranteed Income4Life is an investment plan which can secure an income for you until the age of 99. Since you may want to start this income at the age of 60 or a little later, you can start this plan at the age of 45.

This plan allows you to invest for a few years and then start receiving regular income out of it. This income can continue till the age of 99. If you hold this investment jointly with your spouse, the pension continues until the surviving spouse reaches the age of 99 or natural demise.

Guaranteed Income4Life automatically secures an income for you while you decide where and how much to invest the money from other plans.

Pension plans help you convert your wealth into regular and reliable stream of income. Thus, they are an inseparable part of your retirement plan. Apart from the Guaranteed Income4Life plan, Canara HSBC Life Insurance also offers the following pension plan for your post-retirement income needs:

This is an investment plan where you can invest the lump sum money received from other long-term investment plans to create pension income. You can invest in the following options depending on when you want your income to start:

Know more about Pension4life.

Fixed deposits are one of the most popular and perhaps one of the easiest to use investment options. Especially if you have little time to look at where your money is going. Fixed deposits offer the following features, benefits, and limitations to your money:

National Pension Scheme or NPS is a perfect retirement investment solution that you must have in your retirement portfolio. The major advantage that NPS has over other investments is that you can keep increasing your regular savings in NPS along with your income growth.

Thus, your retirement savings keep up with your income growth without having to buy a new plan now and then. However, the maturity value of NPS is not entirely tax-exempt, unless you follow the withdrawal rules:

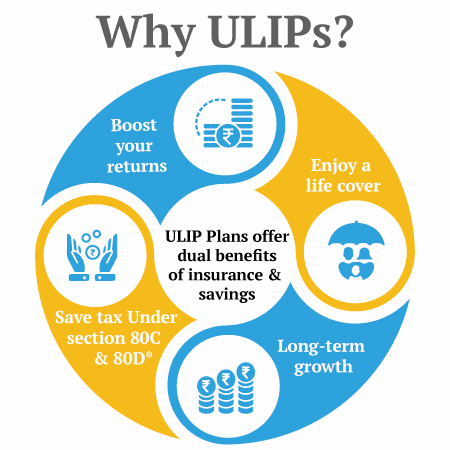

Unit Linked Insurance Plans are a versatile investment option from the life insurer’s portfolio. This is one investment plan which offers a complete portfolio management platform for your investment. You can invest in multiple funds with different risk-return profiles and manage your portfolio like a professional.

Here is the online ULIP plan from Canara HSBC Life Insurance:

Invest 4G is an online Unit-Linked Insurance Plan from Canara HSBC Life Insurance. As a ULIP, it offers two major benefits for retirement savings:

The two benefits ULIP investment offers towards retirement goal are important for you to build an adequate retirement corpus in a hassle-free environment. Here’s how:

A. Multi-Asset or Portfolio Investment

As a young investor when you start investing for a long-term goal such as retirement, you want to invest aggressively to maximise growth. However, as time passes you need to reduce your investment risks so that you can preserve the growth.

A ULIP is perfect for a dynamic risk investment for the following reasons:

Benefits of using Invest 4G plan for retirement savings:

For example, you want to maintain a 50:50 ratio of equity and debt in your retirement portfolio. The fund will withdraw from equity funds and deposit to debt funds when the markets are performing better and reverse the flow when the markets are running lower. The transfer will continue until the plan achieves a.50:50 ratio between equity and debt.

Thus, you can take advantage of market movements even when you are not paying attention.

For example, you want to safeguard your returns from the equity funds and decide that any growth above 5% of the folio must be preserved. Thus, every time the value of equity funds grows beyond 5% the plan will move the additional money to the debt fund.

Thus, you can use the strategy to systematically transfer your entire equity corpus to debt and liquid funds in the final four years of the plan.

Bonus Additions – Growth Boosters

Invest 4G offers two bonus additions for long-term investors:

ULIP plans carry a mandatory lock-in period of five years. But, after five years any withdrawals from the plan are completely tax-free. If you have bought a ULIP plan after 1st Feb 2021, complete tax exemption will only apply to the withdrawals if your total annual investments in the plan have been Rs. 2.5 lakhs or less.

The tax-free withdrawals are very convenient when you are close to retirement or after retirement.

You can ensure a financially independent life post-retirement by investing appropriately in a couple of these plans. Also, these investments would offer tax relief which means additional savings. Remember that every investment plan will allow you specific benefits. So, invest as per your needs.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.