Written by : Knowledge Centre Team

2021-11-10

871 Views

Share

There is no doubt that the 21st century has witnessed great hype in competition due to globalization and the digital revolution. As the world is changing rapidly, the trends in financial planning are also changing. Gone are the days of the old-school thought when people would dedicate their entire career to an organization and then retire with a nice pension and gratuity. Today’s go-getting individuals seek the best retirement plans to boost the savings corpus. In such a situation, you might have asked yourself - “How much money do I need to retire?”

Indeed, this is a frequently asked question among the millennials - i.e. those who were born between 1981 and 1999 and have grown up as adults in the Millennium 2000. Not to forget, this generation has been those of the trend-setters.

Being exposed to various challenges and economic crises, they have been a part of the digital revolution.

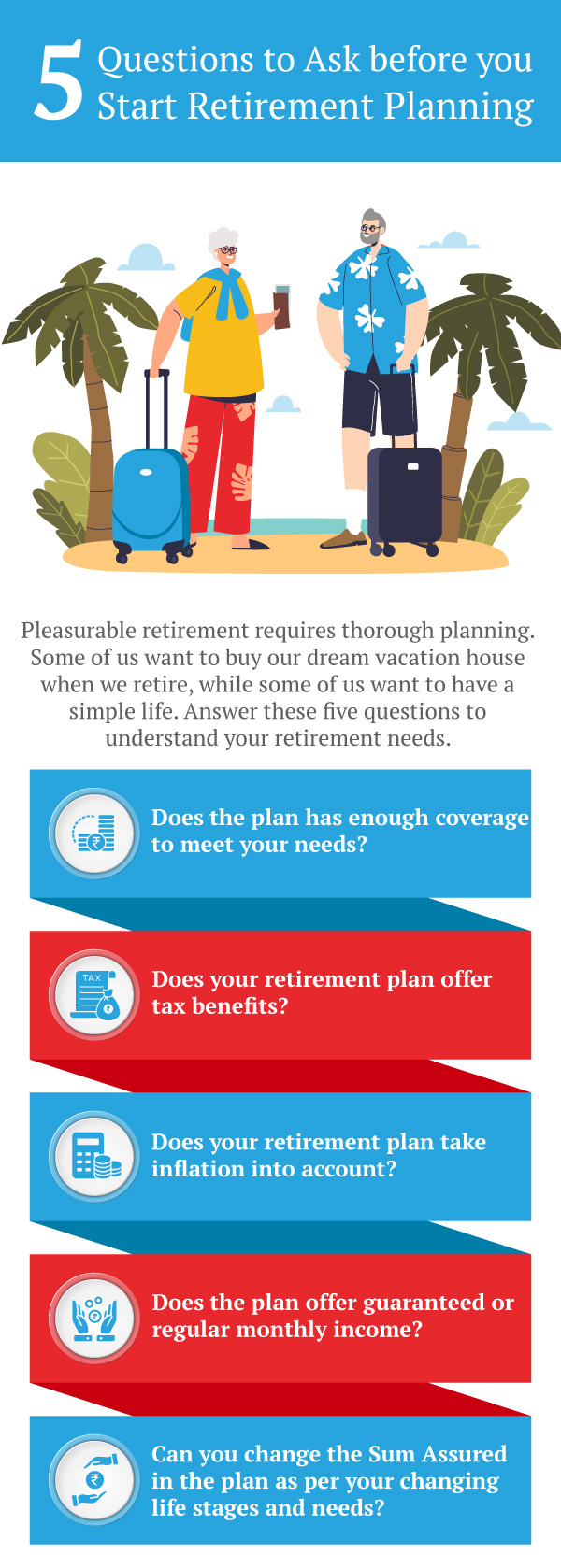

Based on your annual income, you can easily figure out how much retirement savings you need for a comfortable life. You need to chalk out a plan to save a part of your annual income into a savings plan that can yield sufficient returns at the prevailing ROI.

To understand better how to save for retirement, you may refer to the case study given below:

Varun is a 30-year-old fin-consultant working in a leading fintech concern based in Delhi. He is earning an annual package of ₹ 12 lakhs. His ambition is to buy a small plot of land in Dehradun and build a luxury villa and live a comfortable retirement life over there. No doubt, he requires a lot of savings to fulfil his dream.

Taking into account the prevailing return of investment i.e. 8%, if Varun’s income is increasing at the rate of 5%, there can be 3 different scenarios:

He saves 9% of his income towards a profitable retirement plan such as a ULIP, he will have to save around ₹ 1.08 lakhs in the initial year. Over the next 30 years, he will be able to build a savings corpus of over ₹ 2.28 crores.

If he saves 18% of his income towards his retirement plan, he will be able to build a corpus of over ₹3.06 crores over the next 30 years. In this case, Varun had started withdrawing his savings at the age of 55 to fulfil some of his long-term goals like paying off an outstanding loan or paying for his child’s education.

Similarly, if he saves 34% of his income towards retirement, he will be able to build a savings corpus of over ₹ 3.9 crores by the time he turns 60. In this case, Varun had started withdrawing his savings at the age of 50.

Based on the risk appetite, you may opt for one of the following types of retirement investments:

If you are salaried you may have an ongoing contribution to Employee Provident Fund or National Pension Scheme. These are completely tax-free retirement investments. This contribution ranges from 10 -12% of your monthly income including your employer’s contribution.

You can claim the tax deduction u/s 80C of Income Tax Act on your contributions towards EPF and NPS. However, you may be able to reap limited financial growth with these savings instruments.

EPF and NPS can take care of your bare minimum retirement saving needs. However, it is important to invest an additional amount for the safety of your goal. ULIP plans can be a good option in this direction.

ULIP plans offer you the opportunity to select your investment portfolio among equity, debt, mutual funds, and hybrid funds.

Moreover, you can readjust your portfolio with various portfolio management strategies. Invest 4G offers four automatic portfolio management strategies:

This makes ULIP a truly investor-friendly plan. What’s more, in ULIP you can earn loyalty bonuses for your long-term investment in the policy.

Furthermore, if you wish to get a tax-free income after retirement, you may select the Century option in the Invest 4G Plan.

In this case, you can continue the policy till the age of 100 and start systematic withdrawals at 60. All your withdrawals from a ULIP plan shall be tax-free u/s 10(10D) of the Income Tax Act. You will also receive the remaining fund value if you survive the policy term.

Guaranteed Savings Plan are a good idea if you want to invest safely but want better growth for your savings. Canara HSBC Life Insurance Guaranteed Savings Plan. This will offer you a risk-free investment opportunity.

Above that, you can even avail of the Milestone Withdrawal Option on this plan. In this option, 20% of the available fund value on the date of payment will be given to you at the end of the 10th Policy Year and every 5th year thereafter. Such withdrawals are tax-free.

If you seek regular income after retirement, Canara HSBC Life Insurance Guaranteed Income4Life is the right option for you. You can choose this plan if you are 40 years or above.

Here you can choose between the long-term income option of 15 or 20 years, or the lifelong income option till 99 years.

These are the various ways how to save for retirement with better financial growth.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.