Locate branch

Resume journey

Pay Premium

Contact us

Until about two decades ago, retirement was defined by the employer and their employees were not allowed to work after this age. The age was initially fixed at 58 for several years and then subsequently revised to 60 years.

With increasing life spans and opening up of a plethora of opportunities in a modern, liberalized Indian economy, people have the freedom to choose their retirement. Whereas some people decide to hang up their boots when they feel financially secure, others keep working until their health permits them to do so. But in either case, you need to start saving for your retirement as early as possible.

How to Begin Planning for Retirement?

If you have just started earning, it would be too early for you to judge what you would like to do. However, it’s always better to stay prepared for the most commonly expected future, i.e., retiring at 60 and living through 85.

As per a report titled, The Future of Retirement, the Cost of Ageing, by HSBC, 56% of the working population lives paycheque to paycheque, putting themselves at grave risk for the future. However, the reality is that most do not realise how important this goal is until they are very close to it.

Also, it’s not very difficult to start your retirement plan. Just keep in mind the following:

- Retirement plan works on the principle of ‘income replacement’. So, if you are earning Rs. 30,000 right now, you should save to have this income as your post-retirement pension.

- You should start investing at least 10% of your monthly income towards retirement. 15% is the best ratio you can get.

- Consider higher savings as the scenario for employment keeps changing and you may face periods of unemployment. Inflation is another factor that you must consider. So, higher savings will keep it covered.

Where to Invest for Building a Retirement Corpus?

Initially, your investments may look timid, but the fund will grow over the years if you choose the right savings plans. Remember, you are saving to replace your current income. So, your annual savings will be limited to a percentage of your income.

To start you can save 10 – 15% of your monthly income into any of the following investment options:

1. Employees Provident Fund (EPF)

The EPF, commonly called PF, was launched in the 1950s as a retirement planning scheme for employees working in organizations with more than 20 staff members. A fixed percentage was deducted from the employee’s salary each month and transferred to the EPF account. The employer had to also contribute an equal amount to this PF kitty.

The government of India adds interest to this amount. This compulsory saving scheme ensured financial discipline and built a retirement fund for the employee. PF contributions are also attractive because they are deductible from taxable income.

Let us consider an example, if the basic component of your salary is Rs.15,000, about 12% of this would be your contribution to the PF fund. If you started contributing to PF at the age of 30 and expect to retire at 60:

| Values | Employee Contribution (@12%) | Employer Contribution (@3.67%) |

|---|---|---|

| In a Month | Rs.1,800 | Rs.550.50 |

| In a Year | Rs.21,600 | Rs.6,606 |

| In 30 Years (with 5% Annual Increase in Basic Income) | Rs.15,28,435 | Rs.4,67,443 |

| Total Contribution | =Rs.15,28,435+Rs.4,67,443=Rs.19,95,878 (Average of Rs.66,529 per year) | |

| Fund Value In 30 Years (with 8.5% Rate of Interest) | Rs.69,97,411 (Approx. Rs.70Lakhs) | |

2. Public Provident Fund (PPF)

PPF is a Central Government guaranteed investment cum tax saving instrument, still considered to be one of the best options to deliver inflation-beating returns. The current rate of interest is 7.1% and is a safe option if you are looking at risk-free, stable returns in the medium-to-long term.

You can open a PPF account at select bank branches and post offices. PPF account has a minimum tenure of 15 years and can be extended in blocks of 5 years after maturity.

The amount deposited in PPF accounts is eligible for deduction under Section 80C. Whereas, all withdrawals are exempt from taxes. However, partial withdrawals are permitted only from the 7th year onwards. A minimum annual deposit of Rs.500 is mandatory to keep the account active.

If you start investing Rs.67,000 every year starting from the age of 30 and decide to keep the account running until you turn 60, you will earn a lump sum amount of Rs.69,00,000 (Rs.69Lakhs).

3. National Pension Scheme (NPS)

NPS is a voluntary pension scheme that is exempt from taxes both at maturity and annuity (up to 40%) stages. Contributions to NPS are also deductible, under section 80C, from taxable income. In addition, under section 80CCD(1b), contributions of another Rs. 50,000 are allowed for deduction from taxable income.

If you start investing Rs. 6,000 each month from the age of 30, you will build a retirement kitty with NPS, that will grow to approximately Rs. 74 lakhs by the time you turn 60. You can opt to withdraw 60% of the corpus or stay put and receive a pension each month. If you decide to hold the entire 100% for receiving the pension, you can expect around Rs. 40,000 each month.

Besides these legacy plans, you can also explore wealth generation plans that can grow some of your investments aggressively during the same period. This ensures you have Unit Linked Insurance Plans, Saving Plans with Guaranteed Returns in your investment portfolio. Here are some top retirement and pension plans offered by Canara HSBC Life Insurance.

i. Guaranteed Savings Plan

Guaranteed Savings Plan is a comprehensive instrument designed to meet multiple objectives such as wealth creation, insurance cover, and tax benefits. All investments are deductible under section 80C, from taxable income. In case of untimely demise of the policyholder, the family gets higher of the following as a lumpsum amount.

a. 11 times the annual premium

b. 105% of premiums paid until the death

c. Sum Assured

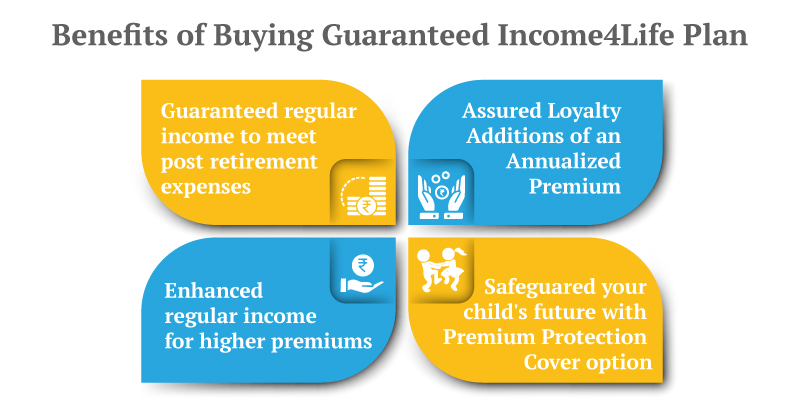

ii. Guaranteed Income4Life

A perfect saving and investment plan if you are looking for an income stream to match a future expense, such as post-retirement. You can choose to invest for a specific period (say 10 years) and defer the pay outs by another 5 years.

Your pay outs will start thereafter. You can also opt to receive the future regular income pay-outs as a lump sum calculated as the current value of the amount.

The policy also offers some valuable additional features under the premium protection option. Premium protection will financially secure the goal in case of your death or disability within the policy tenure. Some key highlights of Guaranteed Income4Life are:

- Future premiums are waived off in case of untimely demise or permanent disability.

- In case of untimely demise, the family will receive the sum assured immediately. The family will receive the fund value at the time of maturity-either in regular income streams or as a lump sum

iii. Pension4Life

Pension4Life plan of Canara HSBC Life Insurance is one of the safest long-term investment plans that offers:

1. Immediate Annuity: The pension starts as soon as you invest a lump sum amount

2. Deferred Annuity: Invest gradually and start a regular stream of income a few years later

If you have recently retired and would like to invest a lump sum amount to earn a regular income, the immediate annuity will meet your requirement. If you have a long way to go before you retire, a deferred annuity gives you time to invest over the years and build a corpus.

You will get income streams called “annuities” till the end of your life after which the purchased/invested amount would be given to your nominee. In case you have opted for a Joint Life Annuity, your spouse would continue receiving annuity even after you, until his/her demise. The purchased/invested amount would then be handed over to the nominee.

To summarize, your retirement plan should be balanced keeping in mind your financial goals, security for your family, and your current ability to invest. A healthy mix of high-growth funds and relatively safer instruments will help you build a stable, sustainable retirement kitty that will allow you an equally comfortable lifestyle post-retirement.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

894 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

871 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan