Written by : Knowledge Centre Team

2021-06-07

882 Views

Share

Disability is one of the major risks to your earning capacity. Even though you can eventually recover, it can set you back a few years. The financial side of this risk you can cover with disability insurance. Disabilities range from temporary disabilities to severe permanent ones.

Depending on the severity you may need to change your lifestyle, living space, and commuting preferences. All of these activities require some financial planning. Additionally, you may lose the earnings for the period of recovery or may have to change the profession altogether.

You can have various types of disability insurance. However, the one you should choose for better protection and support will depend on your unique financial needs.

A person is disabled when they have a mental or physical impairment, and the impairment has a substantial effect on their ability to carry out day-to-day activities. This can result in temporary loss of income, reduced income, or a permanent financial dependency. Disability insurance is a protection against the above financial situations.

Since you cannot do your daily activities, you also won't be able to go to work. Based on the type of disability insurance,

a) It can replace a portion of your income when you are unable to work because of disability, or

b) Pay a lump sum amount so that you can meet your medical and household needs

The monthly income helps you meet your regular financial needs and maintain your current lifestyle, while the lump sum is useful for the treatment and other large liabilities.

Short term disability insurance plans can have a waiting period of 0 to 14 days. It allows a maximum benefit period of up to two years.

Long-Term Disability insurance plans can have a waiting period of several weeks to several months. Long term disability insurance benefit can last from a few years, or you can also get coverage for a lifetime.

Insurers classify disabilities based on the magnitude of the impact it has on your regular and earning activities. Below are the different types of disabilities classified in insurance plans:

It is a state where you cannot work due to prolonged illness or bodily injury because of an accident. The disability could be loss of eyesight, speech, or limbs.

It results from an injury or illness that is semi but not fully disabling. Under this, the person can perform some but not all of their ordinary work functions. Or they can do their work activities in a partial capacity and not full capacity. Some examples are - loss of one finger, loss of one leg, loss of hearing in one ear, etc.

When you suffer an injury and can only return to a modified version of your job, it comes under temporary partial disability. It also includes a situation where you can return to another job that involves extremely light work.

It occurs when you cannot move your paralyzed muscles at all. Paralysis can occur in a limb or multiple limbs. The worst case of paralysis could be that the body itself is paralysed and bedridden. Your insurance may treat double limb paralysis as permanent total disability.

| Disability Insurance – Type | What is it? |

| Accidental Disability Insurance | A disability that arises due to an accident is covered under these insurance plans. Under this, you get a certain percentage of the sum covered depending on your insurance plan. |

| Critical Illness Insurance | These plans provide a wide range of cover against specific life-threatening diseases like cancer, stroke, kidney failure, etc that impact your day-to-day work. |

| Short-Term Disability Insurance | These cover you for a limited time. The waiting time for most short-term disability insurance is 14 days, and benefits are limited to a maximum of two years. You continue to receive benefits until you have recovered or exhausted the coverage amount. |

| Long-Term Disability Insurance | Under this insurance plan, you can continue to receive benefits for a few years or your entire life. The waiting period can be a few weeks to months. |

When you opt for disability insurance, you get cover for disabilities as per your disability plan. The disability insurance works as below:

a) You make regular premium payments to keep your policy active

b) During the policy tenure, if you suffer from a disability due to an accident or illness, the insurance company will pay you an amount based on the severity of the disability. For example,

c) Comprehensive disability policies may also pay you a monthly benefit in the case of Temporary Total Disability.

d) The best disability insurance plans offer increasing cover for the claim-free years. That means, your sum assured will keep growing until one of the following occurs:

There are many options when it comes to disability insurance. The first thing you need to do is assess your situation. Before buying disability insurance - consider your liabilities, and evaluate your family's financial situation. Based on the data, determine the appropriate coverage level you will need, and then start to look for disability insurance.

Below are a few things you should look for in a disability insurance plan:

Your ideal disability insurance will cover disabilities from any insurable cause, i.e., accident, illness, etc.

It is better to add your disability cover to a term life insurance. It will allow you to benefit from the premium waiver option. Meaning, that once the insurer accepts your disability claim, your remaining life cover premiums will be waived off.

Choose a plan that offers you lumpsum payment and regular income benefits. While a lump sum amount helps you meet your treatment and lifestyle change costs, the regular income can take care of the household budget.

In a disability condition, your medical needs may increase with time. Hence, look for insurance that comes with an increasing cover option to take care of increasing medical costs.

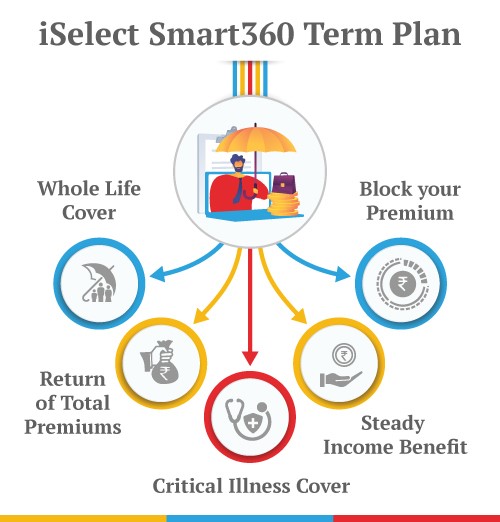

iSelect Smart360 Term Plan is an online comprehensive term insurance plan that offers life cover till 99 years along with disability cover. Future premiums will be waived off if the policyholder is diagnosed with critical illness (listed 40 critical illnesses) or in case of accidental total and permanent disability, if opted.

Having adequate insurance like term and health insurance is a must for your contingency plan. However, there are specific life events that can completely ruin your planning. Hence, it is essential to have other covers as well.

Understand the types of disability insurance and critical illness insurance as well. Investing a small amount in these insurances will help you with solid financial safety for your loved ones. You can enjoy your life without worrying about unexpected life events.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.