Locate branch

Resume journey

Pay Premium

Contact us

When you are young, retirement is at yonder and looks like loads of fun. But did you know that the vast majority of senior citizens endure retirement, not enjoy it? Needless to say, health-related issues are one of the major woes afflicting the older population. But money is a bigger challenge. Financial insecurity is the biggest impediment in leading a comfortable retired life. There are a lot of investment options that are essential for a comfortable retirement.

Majority of the working population lives paycheque to paycheque, putting themselves at grave risk for the future.

Ergo, there are three challenges that, if addressed early in life, can make retirement financially comfortable:

i. Saving

ii. Investing

iii. Wealth Creation

How much Money do you Need during your Retirement?

Considering the overall inflation rate to plan for retirement could be detrimental. You must consider what will remain relevant to you over the years. Both healthcare and food costs account for a major portion of senior citizens’ living expenses.

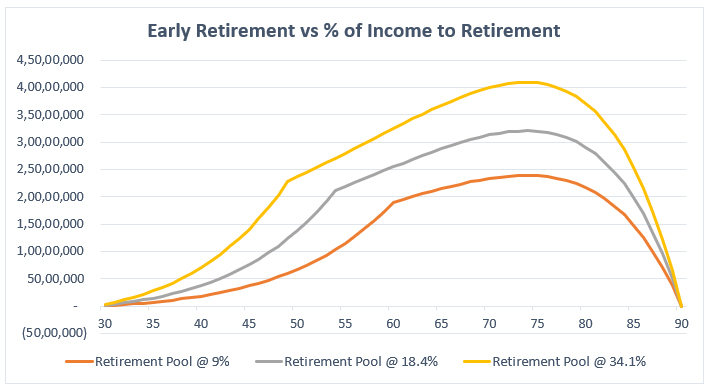

Figure 1: What percentage of your annual income should go to your retirement?

You can consider the complicated estimates and time value of money, including the inflation and rate of return on your investments. However, it all boils down to one simple factor – what percentage of your income are you saving towards your retirement?

Learn the top mistakes to avoid while planning for your retirement.

Figure 1 shows the accumulation and depletion of retirement corpus built at different saving ratios. Here’s what it shows:

- Let us assume that you start investing 9% of your income towards your retirement, at the age of 60 the corpus will be sufficient to provide you until the age of 90

- Similarly, Investing 18.4% of your income towards your retirement will enable you to retire at the age of 55 and continue comfortably until the age of 90

- And, investing 34.1% of your income for retirement, will allow you to retire at the age of 50 and the corpus will be sufficient to provide for you until the age of 90

Provided…

- You start withdrawing the approximately same amount of money you used to earn at the age of 30

- Inflation, income, and pension growth is 5% p.a.

- Your rate of return on the invested money is 8% p.a.

This should give you an idea about how much of your income going to your retirement funds will ensure that your retirement is financially secure.

How to Solve Post-Retirement Problem Before you Retire?

Both Saving and Investing may, prima facie, look very similar but are contrastingly different. Putting aside some money each month right from the day you start earning is quintessential. If you do not “save” you will end up with no funds post-retirement. Your regular income streams would also dry up post-retirement.

Investing will grow your money over time. If you invest your savings in financial instruments such as Fixed Deposits (FDs), Public Provident Fund (PPF), National Pension Scheme (NPS), your money will grow at the specific rates of interest as announced by the bank or government. For example, FDs offer rates between 4% to 8% depending on the bank and tenure.

But if you observe closely, both “Saving” and “Investment” will not help you lead a retired life that is equivalent to the quality of life that you are used to, now! Inflation reduces the buying power of your money over time. To ensure your hard-earned money does not erode in value over time, the money must grow faster than the rate of inflation.

Saving Vs Investment: Which is Better?

Effects of Inflation on Your Savings

If you “save” money in non-interest generating assets or allow them to lie around in your savings account:

At the current savings account interest rate (for a savings account) of 3%

Real Return from Savings Account=3%-6%= (-)3%

This is a clear case of erosion where the buying power of your money reduces over time. To illustrate with a simple example:

You buy 2kgs of Oats for Rs 400. In another 10 years, the same 2kgs of Oats may cost Rs 700 at the current 6% rate of inflation.

If you had put in Rs 400 today in a savings account, the amount would have grown to Rs 540 in 10 years. This amount can fetch you only 1.5kgs of Oats then.

Both these examples demonstrate the need to focus on “wealth creation” rather than keeping money aside or “investing” in low-income yielding instruments.

4 Best Retirement & Saving Plans by Canara HSBC Life Insurance

Any investment should be a well-thought-out process keeping in view long-term goals, security of family, and education for children. Canara HSBC Life Insurance offers some of the best retirement plans in India:

1. Guaranteed Income4Life

Guaranteed Income4Life plan allows you to invest for a specific period (say 10 years) and defer the pay outs a few years. Your pay outs will start thereafter.

This plan is perfect for parking funds you receive within the last 15 years of your retirement. Since the plan offers guaranteed income, your investment is not only safe but also turns into a regular stream of income until your natural death.

2. Guaranteed Savings Plan

Guaranteed Savings Plan offers a guaranteed Sum Assured along with guaranteed yearly and loyalty additions. Thus, you can easily estimate your maturity value at the beginning of the investment.

This savings plan is perfect for the occasion when you cannot compromise on the value of the goal and need a guaranteed amount of money. This plan is perfect for wealth preservation before you retire, as the investment gets adequate returns to beat inflation while staying entirely tax-free.

3. Invest 4G ULIP Plan

The Invest 4G Plan, offered by Canara HSBC Life Insurance, is one of the most flexible and efficient investment. It gives you the options to aggressively grow your investment using professionally managed equity funds. In this plan, you can:

- Invest in a mix of equity and debt funds

- Use automated portfolio management to take advantage of market movements and benefit from equity growth even when you are not actively watching the markets

- Boost your portfolio growth with wealth boosters and other bonus additions

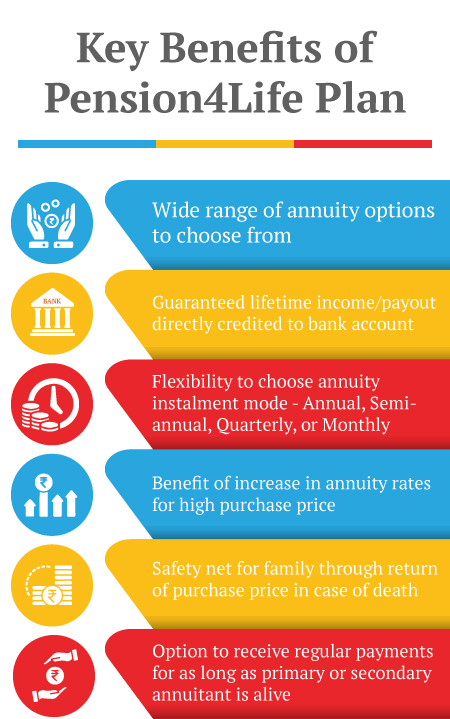

4. Pension4Life Plan

The Pension4Life plan is another safe long-term investment plan that gives you income streams, post-retirement, called “annuities” till the end of your life after which the purchased/invested amount would be given to your nominee.

In case you have opted for a Joint Life Annuity, your spouse would continue receiving annuity even after you, until his/her demise. The purchased/invested amount would then be handed over to the nominee.

Building a corpus considering possible major expenses and cost of living post-retirement helps you plan and start investing suitable amounts starting immediately. Insurance plans help you in wealth creation in the long run as the equity investments beat inflation to give you better returns.

Insurance covers also give you peace of mind because your family would be financially secure in case of your untimely demise. Pension plans offered by Canara HSBC Life Insurance give you a regular income stream even post-retirement to help you have fun in your 2nd innings!

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

893 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

870 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan