Locate branch

Resume journey

Pay Premium

Contact us

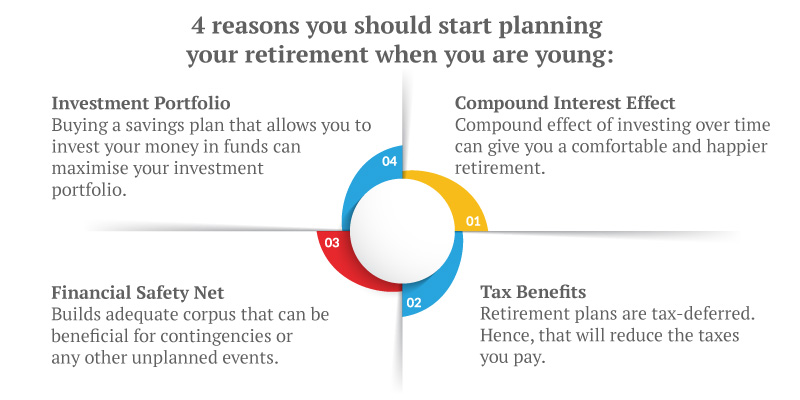

Retirement is a long-term goal. It is not a one-time decision. A lot of thought has to be given to the decision of retiring. It is to achieve the milestone of retirement that you work hard and try to amass wealth.

Thus, planning for retirement becomes an essential part of your work-life. It has to be done more keenly if you are planning to retire early. But before you do look at the pros and cons of early retirement.

Pros and Cons of Early Retirement

Early retirement, unlike other financial goals in life, is a choice with associated advantages and disadvantages. Why would you want to retire early? And why you shouldn’t? Knowing both will help you decide with a little more clarity:

Benefits of Early Retirement

Early retirement does have its’ perks. Also, it depends a lot on the kind of life you wish to lead, and why retirement is on your mind. Below are a few benefits of early retirement.

1. More time for leisure activities

Working for long hours leaves you little time to do any other activity you like. Also, when the time finally comes for you to retire, your health may restrict you from taking part in some activities you may want to do.

2. Time to pursue a new hobby

Early retirement will also be beneficial for you if you look to take up a hobby you once loved or even start a new hobby or activity that you have just thought of and now want to initiate.

3. Good For Health

Job stress is one of the influential factors that deteriorate your health. If you retire early, you will be able to focus more on your health as you will have more time to relax. Less commuting and more peace of mind will also help you stay healthy.

Now that we have taken a look at the advantages of retiring early, this is not always the case. Early retirement has its fair share of challenges as well.

Challenges of early retirement

Early retirement also poses certain challenges. While you want to reap the benefits of retiring early, you should manage these challenges well for a smooth post-retirement life.

1. Savings Needs to Last Longer

The earlier you retire the longer your savings must last to take care of you. Thus, you have to be sure that the corpus created by you will last for a longer period.

Make sure that you budget beforehand, the income you will be requiring.

2. Chances of Restricting your Lifestyle

To retire early, you will save more from your current income to create a corpus large enough to serve you. This will cause you to live in a restricted manner. This cautious lifestyle might not be easy for you.

3. Lack of Things to do After Retirement

The transition phase from the fixed routine of a job to sitting at home can be difficult to cope with as you have a lot of free time after retirement.

So, if you are unable to set a schedule and find something to do, you are likely to get bored and fed up.

4. Inflation

Inflation increases the general price level, so you have to pay more for the things than you used to. This will result in your corpus getting used up faster. So even if you are prepared and think that corpus will be enough that you can retire early, inflation can deter your plans.

Now, the golden question, ‘how do we overcome these challenges?’

Here are a few things you can do.

How to overcome the challenges of early retirement

1. Maintain adequate savings ratio

As discussed above, one fear that arises when you think to retire early is what if you run out of your savings? Well, this can be combated by maintaining an adequate savings ratio.

Ideally, if you can replicate the income which you were earning at the age of 30, into the income which you can withdraw from your corpus when you retire, you can live well.

Suppose you decide to plan your retirement starting from 30 years (the earlier you invest, the better your corpus will be). Then to retire at 60, you will need to contribute at least 10-12% of your annual income to your retirement corpus to ensure a safe retirement.

The early you want to retire, the higher your savings ratio

The amount you want to set aside for your pension fund keeps increasing the earlier you want to retire. For example, if you decide to retire 5 years earlier, that is at 55, the percentage of annual income you have to contribute to the fund rises to 15-20%.

If you retire at 50, then you would have to contribute more than 35% of your income.

2. Invest in Tax-Efficient Instruments

Taxes eat up your disposable income, and you would like to pay it as limited as you can. So, investments that help you save taxes can help you with this problem. Here are some tax-saving instruments offered by Canara HSBC Life Insurance

- Invest 4G

- Guaranteed Savings Plan

- Guaranteed Income4Life

While the maturity amount, you receive is also tax-free under u/s 10(10)D of the Income Tax Act 1961. Not only the maturity amount, but the sum assured that your family will receive after your death is also tax-exempt, that is you are not required to pay any taxes on this amount.

Benefits of Using ULIP for Retiring Early

Above we discussed the tax benefits that ULIP offer to you. But that is not its only benefit. So if you are planning to retire early, ULIP may be your best bet. Here’s why

1. Can Offer Better Growth to Investment

If you want to retire early, you have to make sure that your corpus is big enough to help you sail through those ‘extra years’. To ensure a good corpus, you need to invest in riskier securities, that have the potential to give you better growth over the long horizon.

ULIP policies like Invest 4G, provide you with a range of funds to invest in. All these funds are linked with the market. Investing in equity funds can help you reach your desired corpus faster.

2. Switching Facility

Suppose the market is not performing well, and your investment’s value is going down. Not to worry as ULIP's switching facility allows you to shift your funds between debt and equity. Doing this can help you stay averse to market volatility.

3. Wealth Boosters

Invest 4G also offers certain benefits such as wealth boosters and loyalty additions just for staying invested in the policy for long. Additional units are added to your fund that too at no extra cost. Thus your fund value grows automatically with time.

4. Auto Fund Rebalancing

ULIP helps manage your portfolios via different strategies. One such strategy is auto-fund rebalancing. This allows you to maintain a specific ratio of your savings throughout the term. This helps you when the market is extremely volatile.

For example, if you set a ratio of 50 per cent to debt funds and 50 per cent to equity. Then if due to market conditions, equity becomes 60% of your fund, through automatic portfolio management, your fund will be brought back in the ratio you intended

5. Partial Withdrawal

Under this plan, you are allowed to withdraw your funds. This feature helps when you are in an emergency and need some money If you withdraw after the lock-in period, which is of 5 years in Invest 4G, your withdrawals will also be tax-free.

Many plans such as Canara HSBC Life Insurance ULIP, Invest 4G and Guaranteed Savings plan provide you tax benefits as well. It includes deductions u/s 80C and 10(10)D of the Income Tax Act.

You are eligible for a deduction of up to Rs 1.5 lakhs for the premiums you pay in the policy u/s 80C.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

894 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

871 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan