Locate branch

Resume journey

Pay Premium

Contact us

Are you working on retirement planning for Rs. 5 Crore and working towards creating this retirement corpus? If yes, you are on the right path to building a sustainable future for yourself and your family. But will Rs. 5 Crore be sufficient? It depends on a multitude of factors such as your age, lifestyle, current and projected expenses etc. It also depends on how much can you save diligently to build your retirement kitty.

If you currently lead a modest lifestyle, you will most probably continue the same even post-retirement.

Most organizations have a mandatory retirement age. Even if your health permits you may not be allowed to continue working full-time. Income ceases to exist post-retirement. You will have to still manage your household expenses. Paying bills is possible only if you have a sufficient retirement corpus that can keep giving you cash flows for the rest of your life.

Look at the factors that should shape the size of your retirement corpus:

a) Monthly Rent:

You may like to live in your own house after retirement. However, if you cannot afford to buy one, then you must account for rental expenses in your budget.

b) Household Expenses:

This includes salaries to house help, groceries, toiletries, local travel, water, telephone, internet and electricity etc.

c) Shopping & Dining:

Even though you may vow not to go shopping or buy new appliances, things are going to fall apart. You may end up replacing your washing machine or buying a new set of pyjamas.

d) Health Care:

Your body also needs more care and attention as you age. Expenses on hospitalization, consultations, medicines, medical tests, etc., should be factored into your budget.

e) Vacation:

You may not go exploring the world but you may visit your near and dear ones. Travel expenses should also be budgeted. Of course, you will need more if you are planning exotic vacations that could not materialize when you were young.

How Much to Invest for Building a Retirement Corpus of Rs. 5 Crore?

Let’s say Ramesh is a 30-year-old married man bound to retire at 60. He invests in different asset classes and anticipates a cumulative 12% rate of interest per annum. The inflation rate is hovering at ~ 6%. His monthly expenses are Rs. 50,000 besides an annual expenditure of Rs. 1,00,000 on health and vacation. He expects his expenses to reduce to 75% of his current expenses post-retirement.

Ramesh needs ~ Rs. 5 Cr on retirement. He can either invest ~Rs. 15 lakhs as a lump sum one-time investment or invest ~ Rs. 1.7 lakhs annually for the next 30 years. He can also choose to invest ~ Rs. 15,000 each month for the next 30 years to reach his financial goal.

Where to Invest to Build a Retirement Corpus of Rs. 5 Crore?

Once you have made an approximate budget of how much you may need then, you must carefully evaluate investment options. Some popular options that are used for long-term plans are listed below:

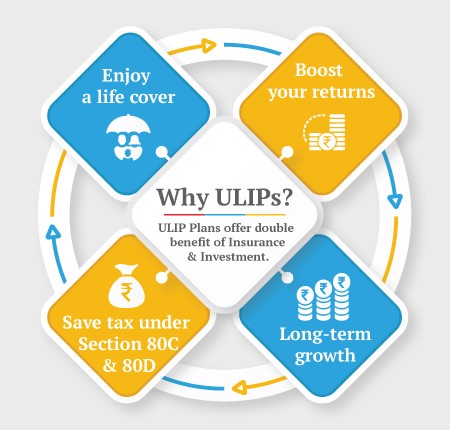

1. Unit Linked Insurance Plans (ULIPs)

ULIPs are solid investment options because you can choose to put your money in diverse funds. Early exposure to equity can help you generate wealth. When you inch closer to retirement, move your money to debt funds to preserve capital. The returns from ULIPs are exempt from tax under section 10(10D).

i. You can invest up to Rs 2.5 lakhs a year in all ULIPs you are investing to keep the returns on them free from tax

ii. Make sure to keep your annual investment in ULIPs up to 10% of the life cover

iii. Switching your money from equity fund to debt fund or vice versa doesn’t attract tax as you don’t need to withdraw the money

iv. ULIPs are more liquid as they allow partial withdrawals after just 5 years of investment

v. Invest regularly and for a long period to enjoy bonus additions to your corpus

vi. ULIPs allow milestone-based withdrawals.

ULIPs like Invest 4G from Canara HSBC Life Insurance allow you to continue your plan till the age of 99. This means you can use the same plan to build a retirement corpus and withdraw your pension. This pension will enjoy tax exemption under section 10(10D) of the Income Tax Act, 1961.

2. Public Provident Fund (PPF)

PPF stands for Public Provident Fund. It is a sovereign guaranteed investment and comes with tax benefits. PPF offers a 7.1% rate of interest. The amount deposited in PPF accounts is deductible, under Section 80C, from taxable income whereas all withdrawals are exempt from taxes. Partial withdrawals are allowed from the 7th year.

i. PPF investment is rather simple, you can invest only up to Rs 1.5 lakhs in a financial year

ii. Invest monthly if you are salaried. However, investing between 1st and 5th April of the year allows you maximum returns.

iii. You can borrow money from the PPF balance in the case of emergencies starting at the completion of one financial year and before the completion of 5th financial year

iv. Make partial withdrawals after the 5th financial year onwards

3. National Pension Scheme (NPS)

NPS stands for National Pension Scheme. Investments in NPS are exempt from taxes both at maturity and annuity (up to 40%) stages. On retirement, you can withdraw 60% of the accumulated corpus and choose to avail pension from the balance of 40%. Contributions to NPS are deductible, under sections 80C section 80CCD(1b), from taxable income.

i. NPS Tier-I account is a pure retirement account

ii. You may not be able to withdraw money before turning 60

iii. You can withdraw for certain milestones or emergencies such as a daughter’s marriage, home construction/purchase, treatment for a specified illness

iv. The best part about NPS is that you can invest as per your income and increase the amount in future when you can

v. Investing in NPS can allow you a tax deduction of up to Rs 2 lakhs in a year

Retire Comfortably with Right Retirement Corpus

Ageing is an irreversible process. Your health, as well as your financial health, are both equally important. Ideally, you should start saving for retirement as soon as you start working. This helps you to invest small amounts and build a huge corpus such as Rs.5 Crore. Basis the retirement age, the monthly investment should also be calculated. This will ensure you remain in a comfortable financial position when you hang up your boots.

Disclaimer: This article is issued in the general public interest and meant for general information purposes only. Readers are advised to exercise their caution and not to rely on the contents of the article as conclusive in nature. Readers should research further or consult an expert in this regard.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

894 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

871 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

875 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan