Locate branch

Resume journey

Pay Premium

Contact us

When 'retirement years' come to mind, we usually imagine a happy and secure life. You spent years working to accomplish your different financial goals and responsibilities. In the second inning of your life, you dream of living a comfortable life with your children, grandchildren and doing what you always wanted to do.

Financial worries should be the last thing that comes to your mind when you think of retirement years, especially if you have already invested in the best retirement plans.

What is an Annuity Plan? How Does it Help After Retirement?

The future life expectancy projections show that with every passing year, the life expectancy will increase. If you plan your retirement with 70 years of life expectancy, the number may be higher when you are near that age (it depends on your current age).

An important question to ponder upon is what if you outlive the years you have planned for. If you spend all your life saving, you will obviously not like to work at that age. The solution to this problem is a life insurance annuity plan.

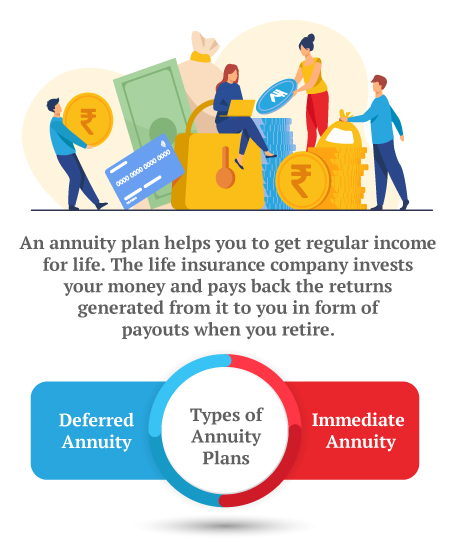

The annuity plan helps you get regular income for life (until your death) in return for a lump sum investment you make today. You can plan for your retirement in different ways, but to handle the above scenario, you may consider having an annuity plan. It will ensure you will always have a continuous source of regular income for life.

For example, Pension4Life plan from Canara HSBC Life Insurance offers a guaranteed lifetime pension which will continue until your demise. You can also get a joint life policy which will continue to provide pension to your dependent spouse after your demise.

How Does an Annuity Plan Works?

An annuity is a long-term investment plan that protects you from the risk of outliving your income. Below are three phases of the annuity plan:

1. Investment

You choose an annuity plan and decide the purchase price in case of a single premium, or you can opt for regular instalments.

You can have up to six annuity options to choose from - you pick the one that works the best for you. You also decide annuity instalment frequency - monthly, quarterly, half-yearly, or yearly. For monthly instalment, you can pay as low as Rs 1000 while there is no upper limit.

2. Growth

If you have opted for the deferred annuity option, you will start receiving the income after a certain number of years. In the meantime, the invested money continues to grow.

The amount the insurance company receives from you is invested in different financial instruments. All the money you invest compounds year after year and finally pays you regularly.

The growth is not taxable. So, even if you choose the safety of capital over the growth opportunity, the investment growth will probably beat inflation by a small margin.

3. Pay Out or Distribution

The insurance company starts to make regular payments. The payment is for life, but in some cases, the pay-out can continue after your death also. For example, when you buy an annuity with your partner. The payment continues till the death of the last survivor.

What happens to your payment after your death depends on the option you have chosen while buying the annuity plan.

Learn what happens to your pension plans after your death.

4. Various Annuity Options

When you decide to buy an annuity plan, you have a number of options to choose from. Each option is different with respect to how your annuity will work after you die. Let us look at the different options.

Although you can have up to six different options for an annuity, there are two major classifications of annuities:

a) Immediate Annuity

b) Deferred Annuity

An immediate annuity begins almost immediately after your investment. For example, if you buy an immediate annuity to receive monthly pension, your first pension amount will arrive one month after investment. Thus, there is no separate growth period in immediate annuity plans.

A deferred annuity allows you to postpone your pension receipt for a while, usually a few years. So, if you defer your annuity plan for 5 years, your first monthly pension will arrive five years and one month after the investment.

| Annuity Options |

| Immediate Life Annuity |

| Immediate Life Annuity with Return of Purchase Price |

| Immediate Life Annuity with Return of Balance Purchase Price |

| Immediate Life Annuity with Return of Purchase Price on Critical Illness (CI) or Accidental Total & Permanent Disability (ATPD) or Death |

| Immediate Joint Life Annuity with Return of Purchase Price |

| Deferred Life Annuity with Return of Purchase Price |

5. Immediate Life Annuity

In this option, you receive the annuity throughout life, and when you die, all the future annuity pay-out ceases to exist. In other words, the policy terminates.

6. Immediate Life Annuity with Return of Purchase Price

You receive the annuity throughout life, and when you die, the purchase price (the price at which you bought the plan) is paid to your nominee.

7. Immediate Life Annuity with Return of Balance Purchase Price

The annuity continues till your natural demise. After your death, the balance is paid to your nominee. The balance is calculated by subtracting the price of the plan and the total of annuity instalments paid till your death. For example, if you bought the annuity plan by making a lump sum payment of Rs 10 lakh and received ten payments of Rs 25,000 each before your death. The nominee will receive a balance of Rs 7.5 lakh as the death benefit. If the balance of purchase price is negative, the nominee does not get any amount.

8. Immediate Life Annuity with Return of Purchase Price on Critical Illness (CI) or Accidental Total & Permanent Disability (ATPD) or Death

Upon your death or if any critical Illnesses is discovered or Accidental Total & Permanent Disability (ATPD) happens, the annuity payment will stop, and the purchase price will be paid to your nominee.

9. Immediate Joint Life Annuity with Return of Purchase Price

This is for a joint account and the annuity continues till one of you is alive. If you die, your partner continues to receive the original annuity amount throughout her/his life. Upon the death of your partner, the purchase price is paid to your nominee.

10. Deferred Life Annuity with Return of Purchase Price

In case of your death, the nominee will receive the higher of below:

a) The purchase price plus guaranteed bonus minus the annuity received till the date of your death

b) 105 percent of the purchase price

The annuity plans like Pension4Life are a great way to live a stress-free life post-retirement. It is not just beneficial for you but also for your partner. You should consider an annuity plan while doing your financial planning for a better and secure future.

How close your dreams get to reality depends on your investment decisions now. One way to achieve it is through Pension or Annuity Plans like Pension4Life.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

Recent Blogs

How to Check Old Age Pension: A Step-by-Step Guide

26 Feb '24

894 Views

Discover the easy steps to check your old age pension status with our comprehensive guide. Ensure a secure retirement with Canara HSBC Life Insurance expert advice and assistance. Stay informed about your pension effortlessly.

Read More

Retirement Plan

Retirement Planning For Working Women

19 July '23

877 Views

Plan for your retirement as soon as you start your first job. Learn how you can plan for your retirement with a savings plan, being a working woman.

Read More

Retirement Plan

Top Investment Options For Retirees?

10 July '23

870 Views

Planning for an ideal retirement? Here are some great investment plans to create your ideal pension after retirement.

Read More

Retirement Plan

Top 3 Mistakes To Avoid While Planning For Your Retirement

10 July '23

871 Views

Top 3 mistakes to avoid while planning for your retirement (1) Not taking inflation into account (2) Not starting early (3) Not building adequate corpus.

Read More

Retirement Plan

How to Plan A Prosperous Retirement with ULIP Investment Plan

03 July '23

874 Views

Whether you have planned your retirement or not, you need to choose good investment options and ULIP can be just the solution for this.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan